2020 was not a usual year, and you may be wondering how it affected the M&A market in our region. With the onset of the first wave of the pandemic in the spring, many were forecasting the M&A market to slow down significantly. The good news is that in our region the annual number of transactions and their total disclosed value ended up at similar levels as in 2019. This result is largely thanks to a strong boost from the region’s thriving startup sector – as many as five of top 10 Baltic deals by value have involved investments in or acquisitions of startups. And on top of that Pipedrive became Estonia’s fifth unicorn!

In this newsflash our Corporate and M&A team takes a closer look at the main Baltic M&A and private equity market trends and shifts over the last year, and attempt to forecast what this year may bring.

Main trends in the Baltic M&A market in 2020

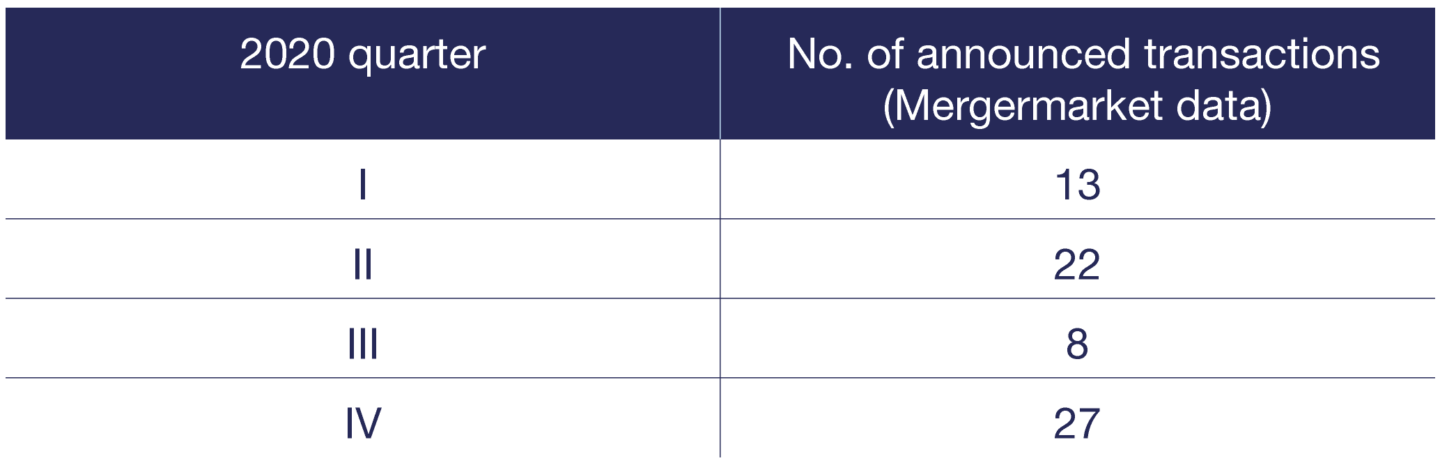

During the first wave some transactions were delayed (though not many were completely cancelled), but at the end of the year the deal market was very active, as both previously delayed transactions and new ones were being closed (see the table below). We actually joked that we had a “double wave” in the M&A market at the end of the year. We are glad that both companies and transaction consultants have quickly adapted to working remotely, and have been successfully negotiating during video meetings and signing and closing transactions online.

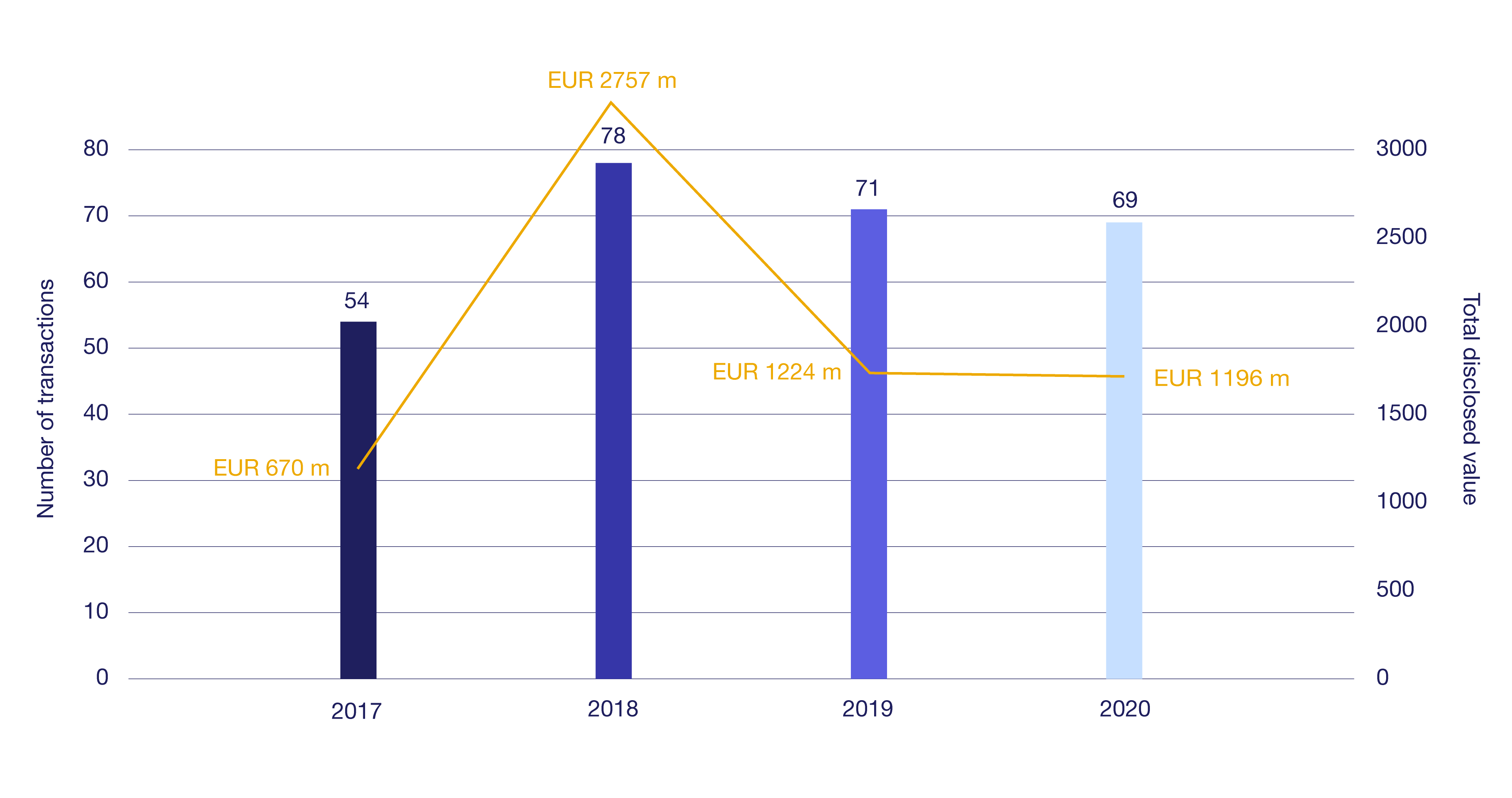

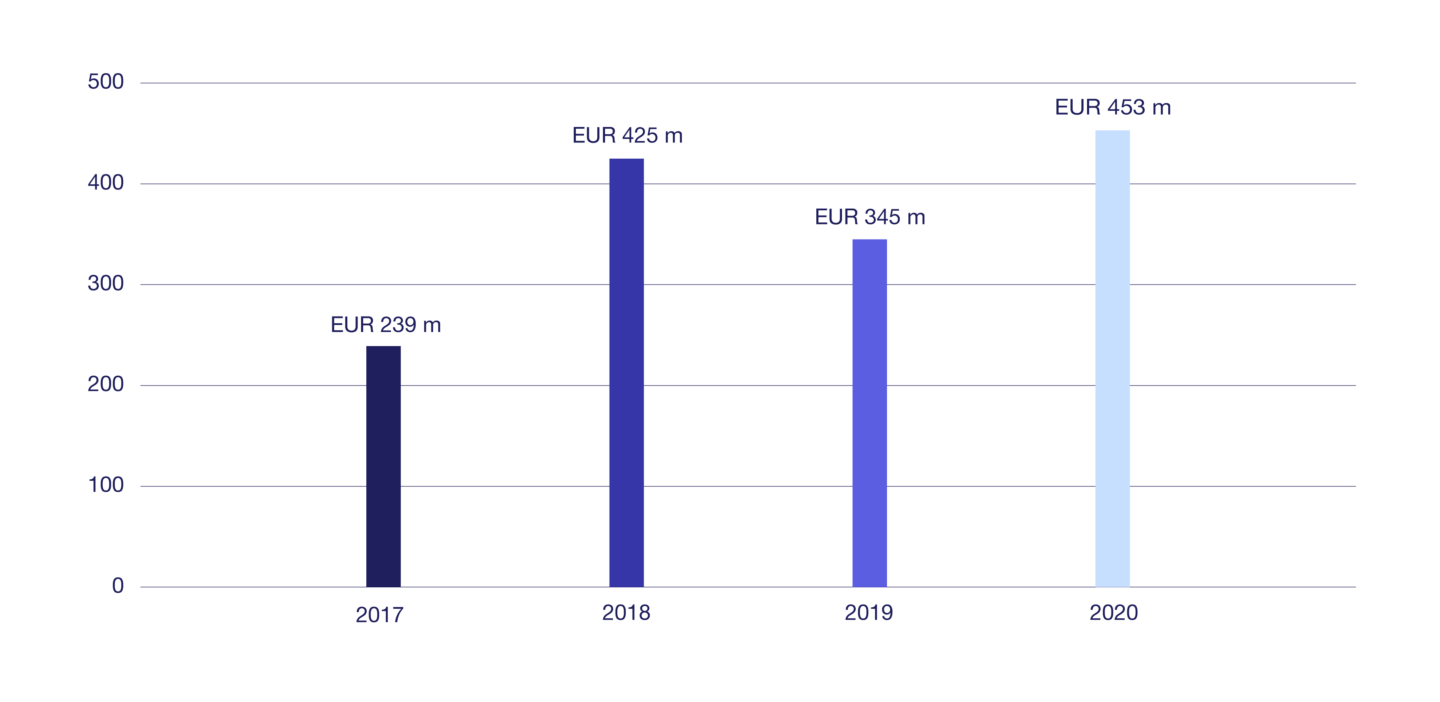

According to statistics from Mergermarket, 69 M&A transactions were announced in 2020 – just two deals fewer than were announced in 2019, when there were 71. The total disclosed value of all announced transactions in the Baltics in 2020 also remained quite similar to 2019 (EUR 1.224 billion in 2019 and EUR 1.196 billion in 2020).

It should also be noted that compared to 2019, in 2020 there were a greater number of larger transactions – we saw six transactions with a disclosed value of over EUR 100 million (in 2019 there were four such transactions).

Number and total disclosed value[1] of announced M&A transactions[2] in the Baltics (Lithuania, Latvia and Estonia) in 2017–2020

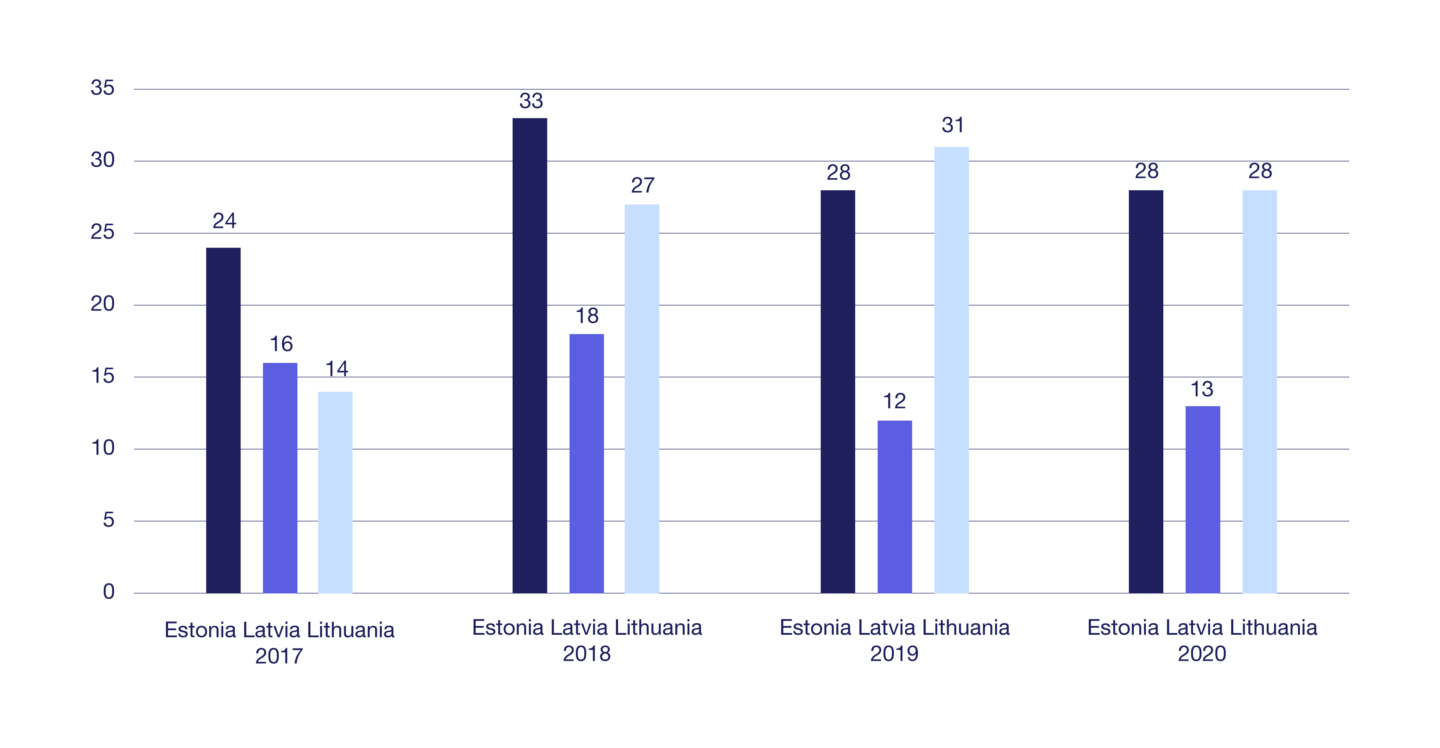

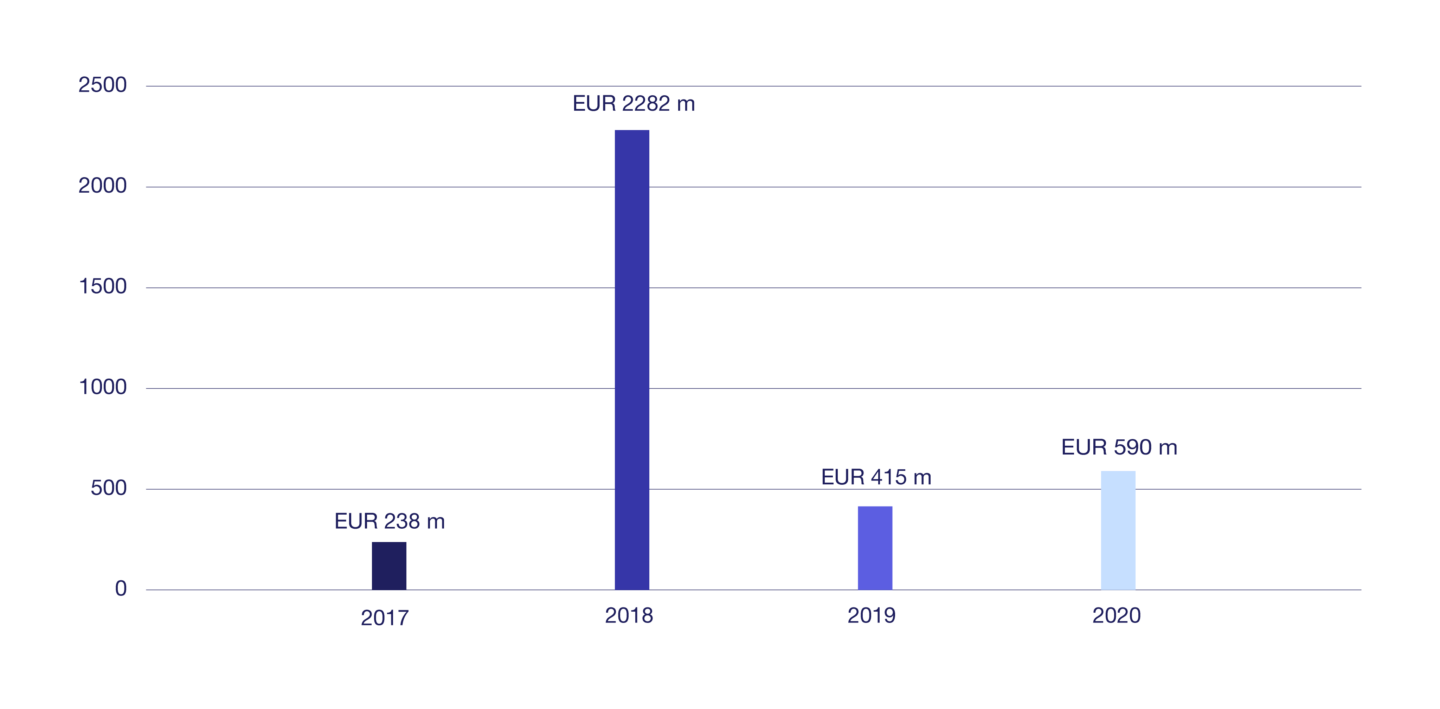

Estonia – Baltic market leader in terms of disclosed value. Although Estonia and Lithuania are tied in the first place by the number of transactions (28 each), Estonia led the Baltic market in terms of disclosed deal value (EUR 590 million).

Number of transactions by country, 2017–2020

Sum of disclosed value of announced transactions in Estonia, 2017–2020

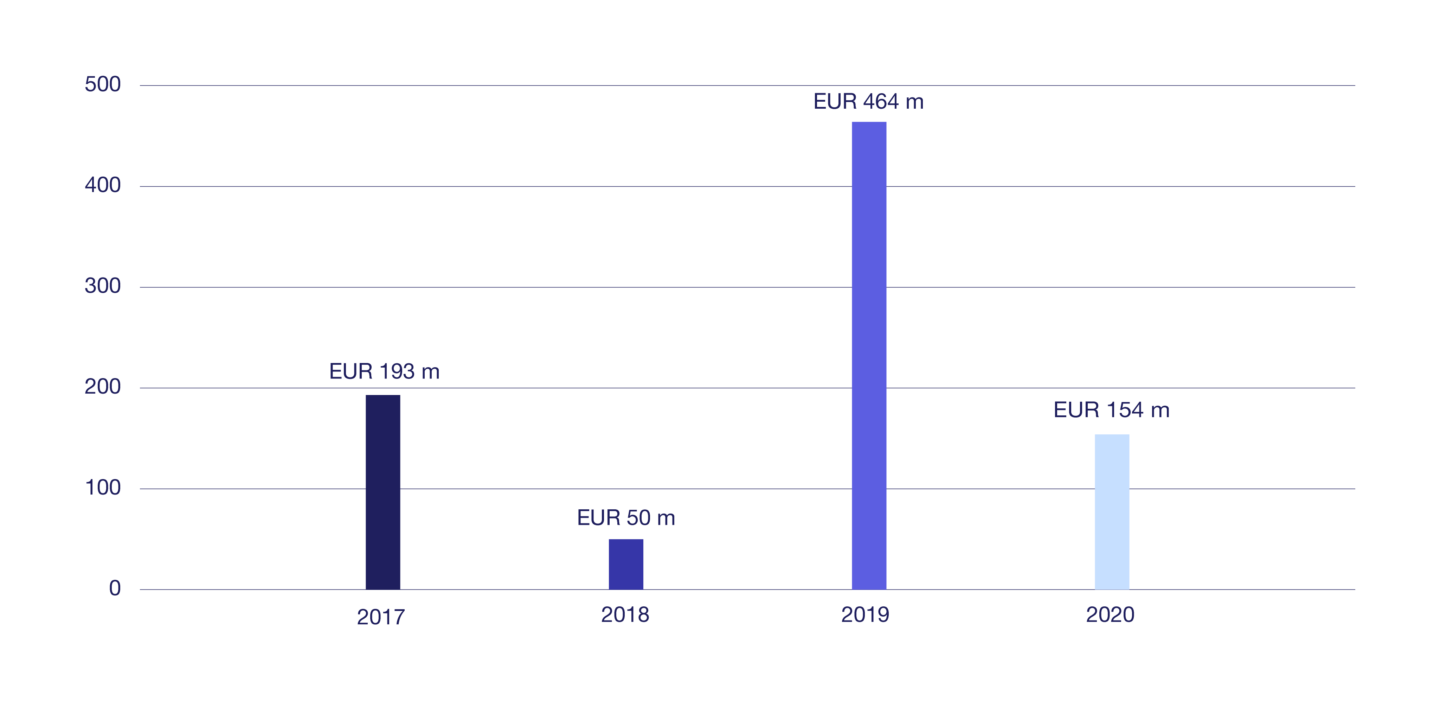

Sum of disclosed value of announced transactions in Latvia, 2017–2020

Sum of disclosed value of announced transactions in Lithuania, 2017–2020

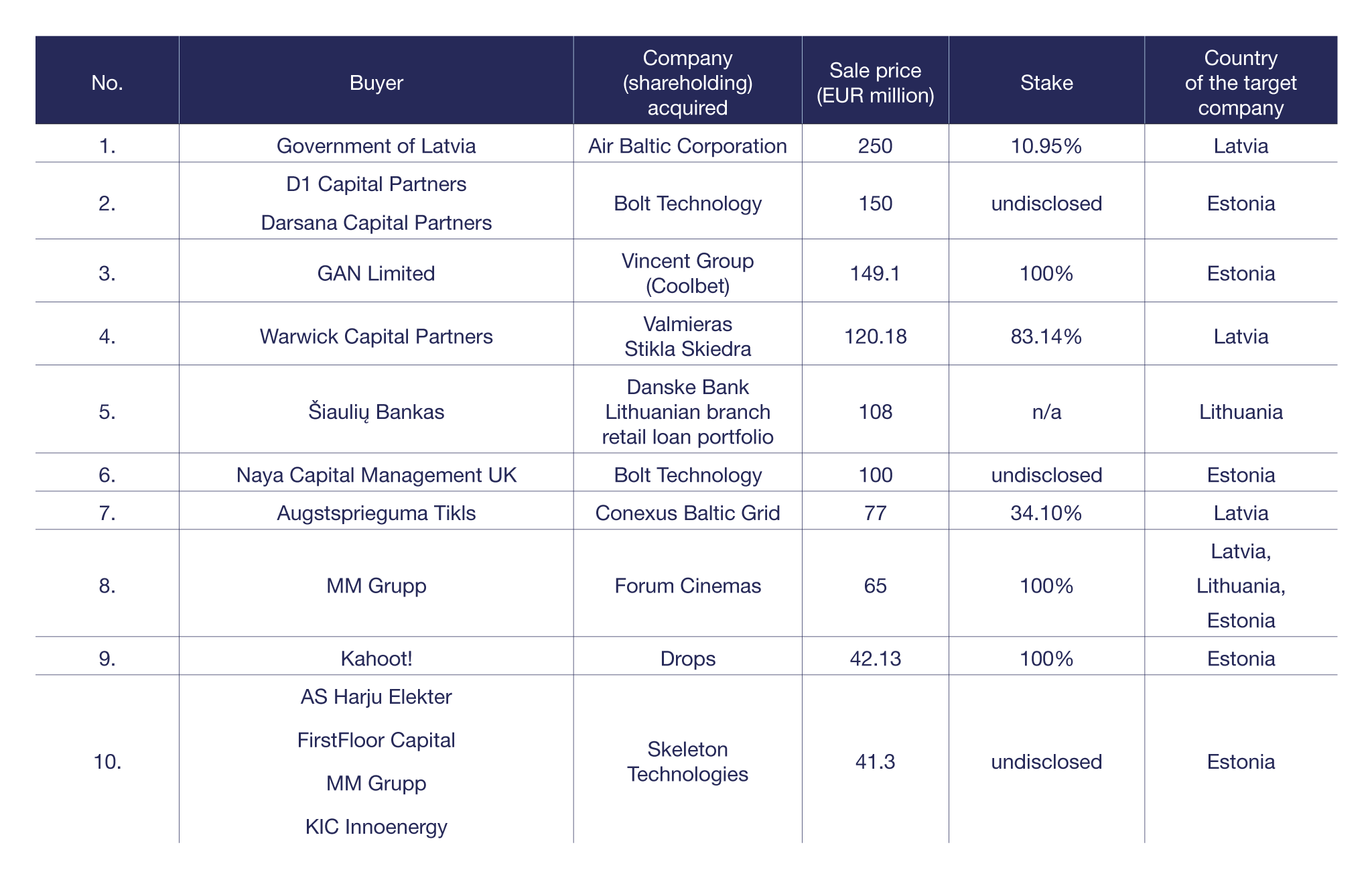

Top 10 M&A transactions in the Baltics in 2020 by disclosed deal value[3]

Most active sectors

The pandemic has accelerated the trend towards the digitalisation of businesses and investment in technology, with the TMT (Technology, Media and Telecommunications) sector being the most active in terms of transactions worldwide in 2020. According to Mergermarket statistics, global M&A transactions in the TMT sector jumped by as much as 56.8% in value (from USD 543.4 billion in 2019 to USD 851.8 billion in 2020).

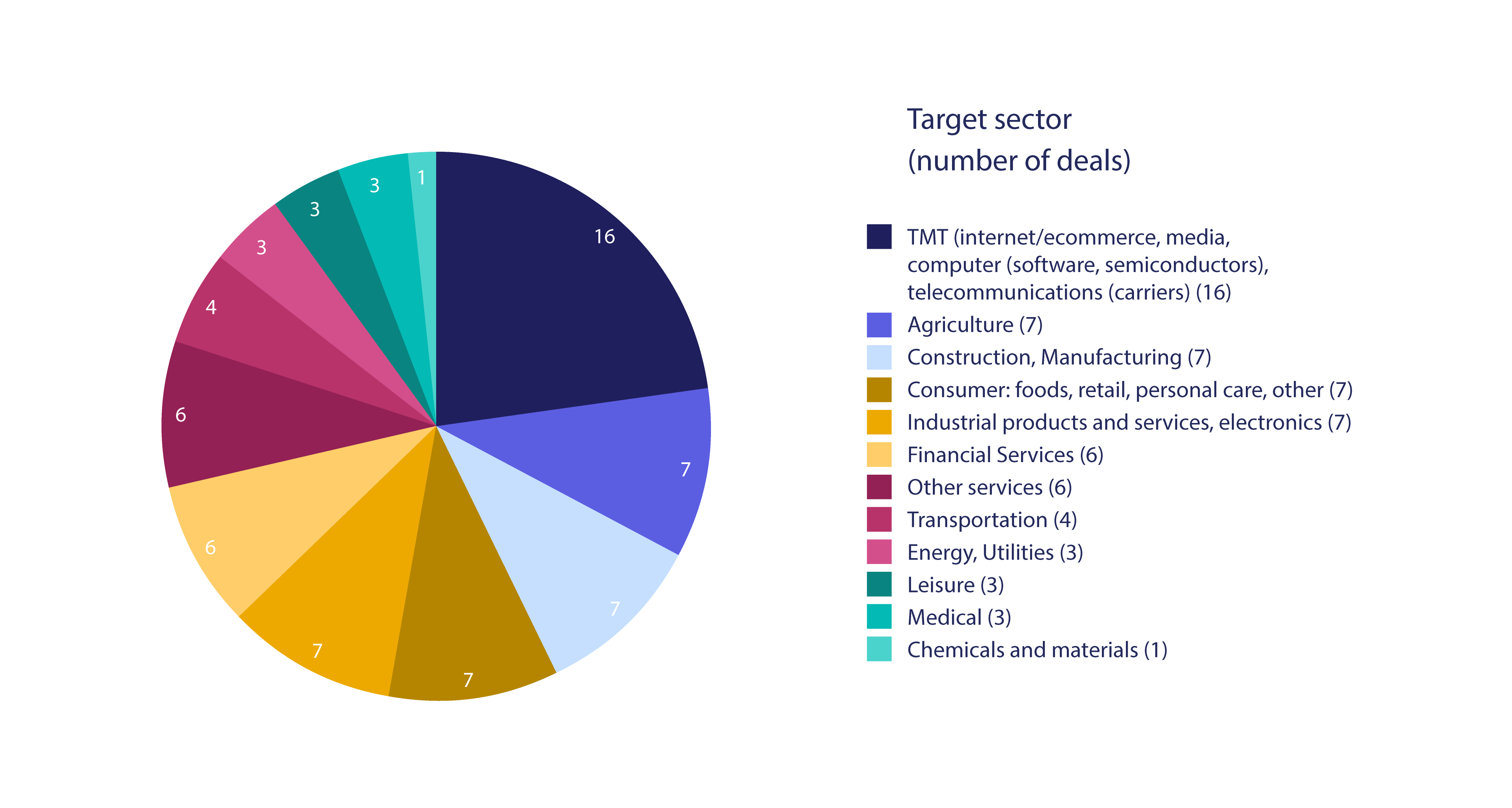

The trend in the Baltics was similar – the TMT sector saw the largest number of transactions (16 transactions) and as many as four of them were among the top 10 transactions by disclosed value in 2020 (No. 2, 3, 6 and 9 in the top 10 deals shown above). We note that the sale of Forum Cinemas (the largest cinema chain in the Baltics, No. 8) could be considered to be a TMT sector transaction; however, Mergermarket classifies it in the leisure sector. Second place (with seven transactions each) is shared by four sectors – agriculture; construction and production; consumer goods and services; and industrial products and services. Being aware of both the continuing focus on TMT globally and the strength of the Baltic startup ecosystem, we forecast that the TMT sector will be highly active this year as well.

Private equity and venture capital market

In 2020, financial investors remained a strong driving force in the M&A market. More than 20% of all transactions involved financial investors, including five of the top 10 transactions by disclosed value.

Record boost from the thriving startup sector! One important point is that 2020 stood out for the record number of investments in Baltic startups. It is the first time to date that as many as five of the top 10 deals by value have involved investments in or acquisitions of startups (Bolt (twice), Coolbet, Drops, Skeleton Technologies). On top of that, in November the Estonian startup Pipedrive received an investment valuing it at USD 1.5 billion, making it Estonia’s fifth unicorn! Let us also remind you that a year ago, in November 2019, Vinted became the first unicorn in Lithuania. We previously forecasted that the Baltic startup ecosystem would gradually start fuelling the Baltic M&A market and its TMT sector. We were wrong about the speed – this thriving sector is already giving a strong boost to the M&A market!

Regional private equity (PE) funds have also been active, and the pandemic has not dampened their willingness to invest. Although none of their deals are among the top ten largest transactions by disclosed value, they have closed remarkable deals that may have broken into the top 10 if their value had been disclosed. What’s more, the size of the largest regional players (primarily BaltCap and INVL funds) allows them to invest in companies valued at EUR 100 million and more, meaning that they can compete for almost all deals on the Baltic market – and that is what they do. In addition to that, the largest private equity houses have not only sufficient size and available funds, but also ticking investment periods, and so we can expect more and even bigger deals from local PE funds in the coming years.

Even if we disregard the largest deals, the venture capital and startup ecosystem in the Baltics has continued to grow successfully. Venture capital funds established 3–4 years ago are gaining momentum and are increasingly often making larger additional investments in their portfolio companies, while also attracting co-investors from abroad or cooperating regionally. At the same time there is still room for new venture capital funds, as evidenced by the launch of LongeVC in Latvia.

Overview of the Belarusian M&A and PE market in 2020

In 2020, the Belarusian M&A market became a law unto itself more than ever before. The effects of the pandemic were overshadowed by the severe political crisis triggered by the presidential election in August, which quickly changed the conditions for both international and domestic businesses operating in the country. Since July, direct cross-border acquisitions and investments have come to an almost complete halt. Some deals that were cancelled were just a few steps away from completion.

The successfully closed transactions relate to various sectors:

- Finance/Insurance: the sale of local operations by ERGO to Euroins, the acquisition of the state-owned Paritetbank by the Cypriot Beristore Holdings;

- Industrials: investment by the German DEG in the only Belarusian manufacturer of gypsum-based construction materials;

- Worth mentioning is the continued investment by leading local private equity fund Zubr Capital in growing local businesses, such as Myfin (an IT platform for banking products) and Realt.by (a nationwide real estate portal);

- Mergers and acquisitions did take place in IT but remained largely non-public. However, an obvious highlight was the acquisition of Melsoft, the developer of the extremely popular Family Island and MyCafe games, by Israel’s Moon Active at the close of 2020.

With the current political turmoil showing no signs of quick resolution and the COVID-19 epidemic still posing a serious threat to the population and economy, the outlook for M&A in 2021 is rather gloomy. We are likely to see some small- and mid-scale local restructurings and acquisitions, some distressed sales and maybe market exits, as well as local assets in various industries, most of all Tech (and especially game development), becoming elements of global M&A deals.

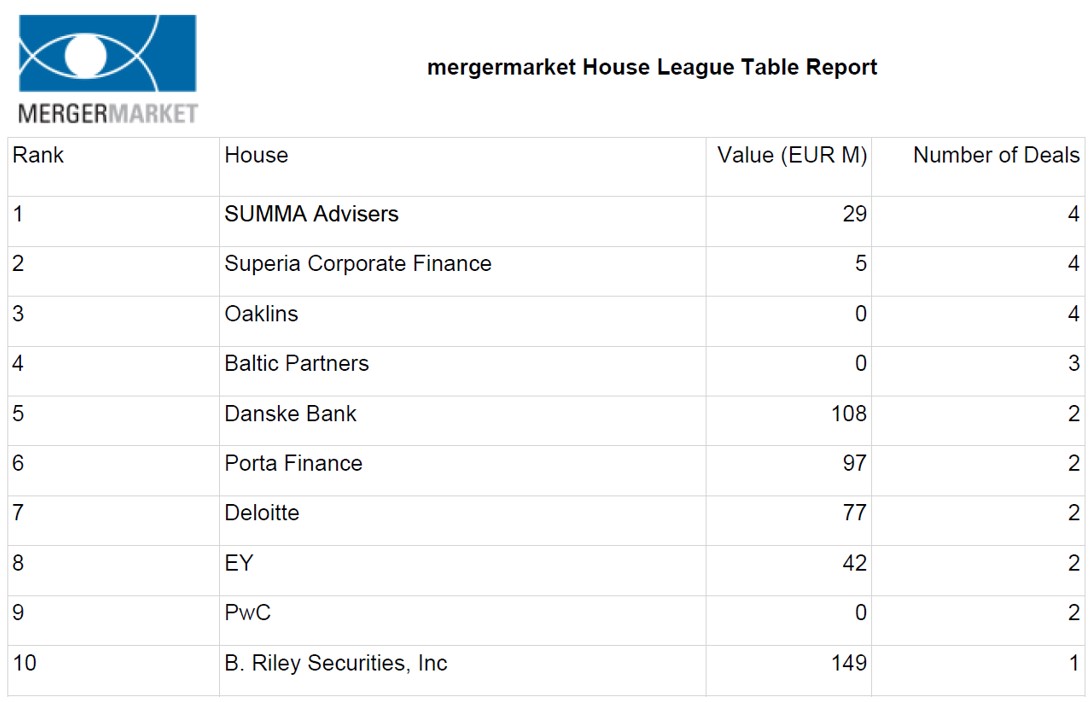

Advisors league tables

Top 10 Law Firms in the Baltics in 2020 (by number of advised deals involving Baltic target companies)

Top 10 Financial Advisors in the Baltics in 2020 (by number of advised deals involving Baltic target companies)

[1] We note that Mergermarket statistics include only values that were disclosed by deal parties to Mergermarket or publicly, thus the numbers in the table may not fully reflect the actual size of the M&A market in the Baltics and indicate general tendencies.

[2] Mergermarket statistics include only higher value transactions (normally exceeding USD 5 million) and do not reflect smaller transactions. Transactions have been assigned to countries based on the “deal dominant geography” criteria in the Mergermarket database.

[3] This table has been prepared based on the information in the Mergermarket transaction database and publicly available data.