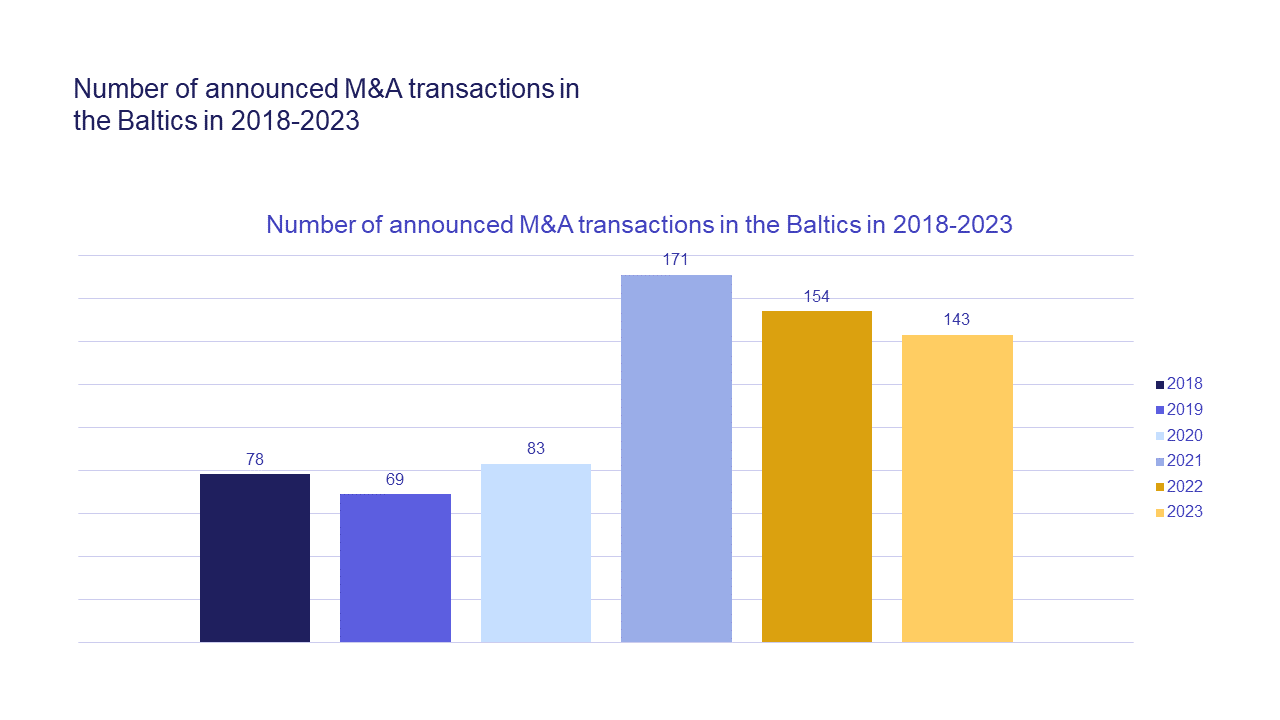

Last year, the Baltic mergers and acquisitions (M&A) market slowed down slightly from the previous year in terms of the number of deals. Despite the minor decline, the numbers still remained significantly above pandemic-time levels, according to statistics compiled by M&A database Mergermarket.

While the deal count downturn wasn’t significant, the total disclosed value of all deals dropped back to 2019-2020 levels, leaving behind two recovery years. Overall, the year saw less large-value deals than in previous years. Of the top 10 disclosed deals by value in 2023, we saw only three deals above EUR 100 million. The year 2022 boasted four deals above EUR 200 million, including the landmark EUR 628 million funding round by Bolt.

Startups dominate the top deals list for the fourth year in a row

Lithuanians go on shopping spree

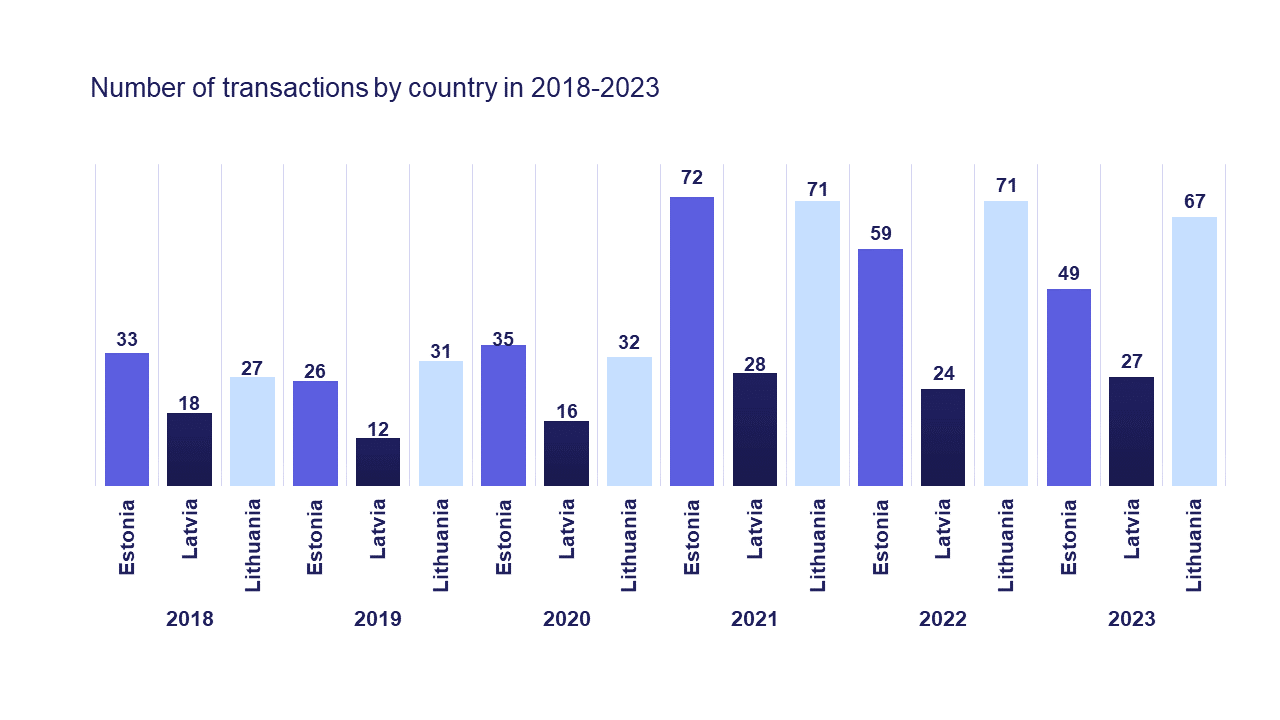

Lithuania and Latvia have retained a stable level of deal activity over the last three years, whereas the Estonian deal count decreased from 72 in 2021 to 49 in 2023. The disclosed deal values declined even more dramatically. This is largely due to a shrinkage in startup financing and a general economic recession in Estonia.

While we keep hearing that foreign investors may be shying away from the Baltic M&A market, the statistics prove otherwise. According to Mergermarket data, in 2020 the share of foreign (non-Baltic) buyers in Baltic company acquisitions was 42%. The number increased slightly in 2021, to 44%, and to 45% in 2022. The percentage went down only slightly in 2023, dropping to 40%.

What is noticeable, however, is that among local (Baltic) buyers, Lithuanian investor activity increased noticeably. Among all the transactions carried out by Baltic buyers, the share of the Lithuanian buyers was 27% in 2020, 43% in 2021, 39% in 2022, and made up almost half of all the deals, or 49%, last year.

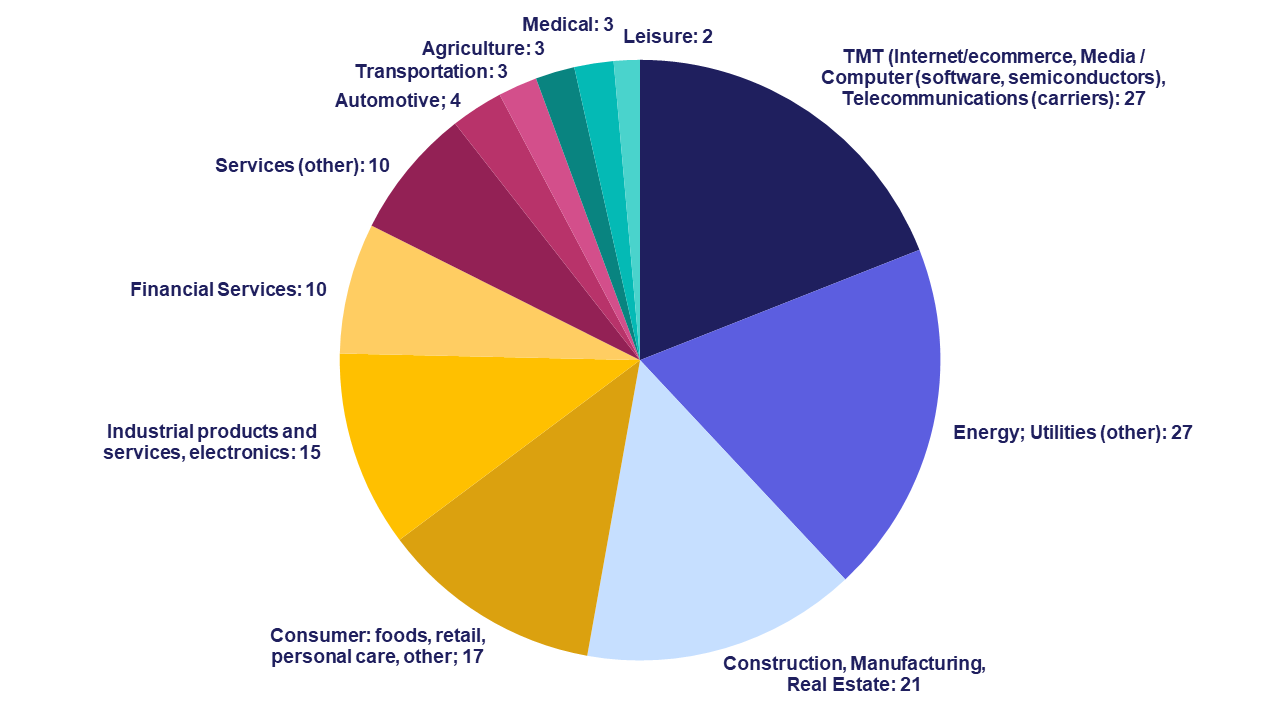

Energy sector catches up with TMT, construction sector not far behind

The top three sectors by deal activity in 2023 were TMT; energy and utilities; and construction, manufacturing, and real estate.

There was a notable increase in the number of energy and utilities sector deals – increasing from 18 in 2022 to 27 in 2023 to share the top spot with TMT. Among the top 10 deals by disclosed value, we see as many as seven energy-related deals – Gaso and Latvijas Gaze (Latvian gas companies), two Skeleton Technologies fundraising rounds (Estonian scale-up developing energy storage technologies), PVCase (solar technology company), Elcogen Group (green hydrogen technology), and Sunly (wind and solar energy park developer).

2024: current activity level expected, with promising pipeline

Sorainen M&A experts expect the total number of M&A transactions to remain at a level broadly similar to 2023. However, a few large transactions could significantly change the scene. In recent months, the plans to sell several large Baltic companies have been announced, including Luminor, Eco Baltia, and Cgates.

airBaltic has announced plans for an IPO during the second half of 2024, and last summer, information was disclosed about a possible Citadele Bank sale or IPO. “We are also aware of several more planned larger sales that have not yet been announced,” partner Laimonas Skibarka shares. “Investment advisors say they have enough work on deals that are likely to be completed during the second half of 2024. If the majority of these deals materialise this year, the Baltic M&A market should be quite active.”

Macroeconomic forecasts mirror this optimism. 2023 was marked as a year of economic stagnation in Lithuania and Latvia and a second year of recession in Estonia. However, economists predict that the Baltic economies should return to growth this year. In combination with a receding inflation and a general consensus that the ECB will soon cut interest rates, we are cautiously optimistic that the Baltic M&A market can expect a recovery.

“Geopolitical tensions are currently acting as both a hindrance and a stimulant for deal making,” Skibarka predicts. As foreign investors and some local investors view the Baltics with caution, company valuations are decreasing, and competition between buyers is dwindling. Some shareholders are considering divesting to diversify risks, or already doing so. This means putting businesses “on the counter” that were not previously for sale.

“Now is a good time for bolder investors to acquire businesses at lower prices while having less competition,” Skibarka notes. He refers to the traditional adage – those who take risks also get to drink the champagne.

He also highlights that the generational change of entrepreneurs as a growing trend. Skibarka notes that first-generation entrepreneurs who don’t implement succession planning – transferring businesses to children or hired executives – will have to sell their companies sooner or later.

No cooling down for energy players and start-ups

In terms of sectors, the energy sector will remain particularly active this year. Numerous renewable energy projects are being developed in the Baltics, requiring large amounts of capital. Energy-related startups and scale-up companies will also remain attractive to investors. If you wish to find out more about the energy sector outlook, join us at the Baltic M&A and Private Equity Forum 2024, which will feature a focus panel on the sector.

The TMT sector will also remain active in the transactions market. We may see some larger transactions in the financial and insurance sectors as well. As the proportion of startups and scale-ups in the top 10 deals table has remained constantly high (7 out of 10 in 2023; 6 out of 10 in 2022), this will not change. There are several reasons to believe so:

- a strong and agile Baltic startup ecosystem

- many unicorn-level and other large and fast-growing startups periodically attract capital or get ready for sale

- the absolute majority of Baltic startups are global technology businesses – affected little by geopolitical risks, they maintain value and keep attracting investors

Venture capital (VC) investors have significant funds available and startup runways are considerably shorter than two years ago. “We expect startup fundraising activity to accelerate in 2024 and we should continue to see many Baltic startups in the annual top 10 deals tables,” partner Toomas Prangli predicts.

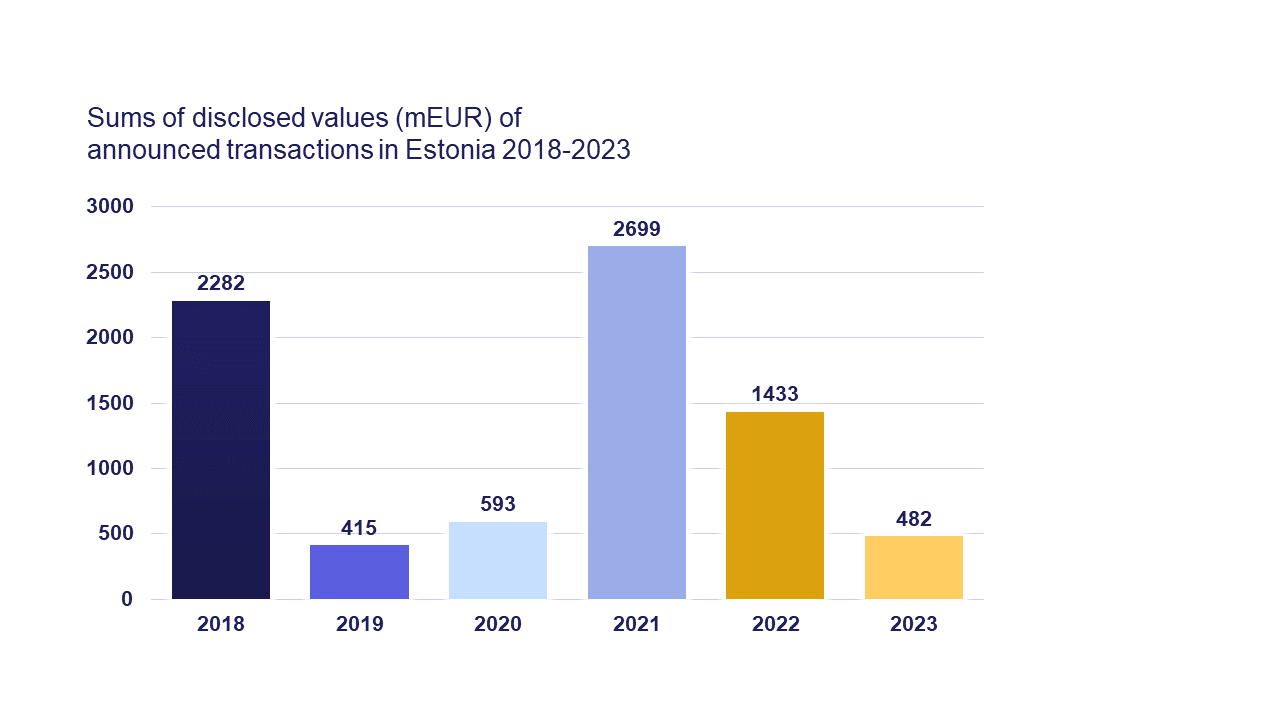

Estonia: recovery hopes despite scary deal value drop

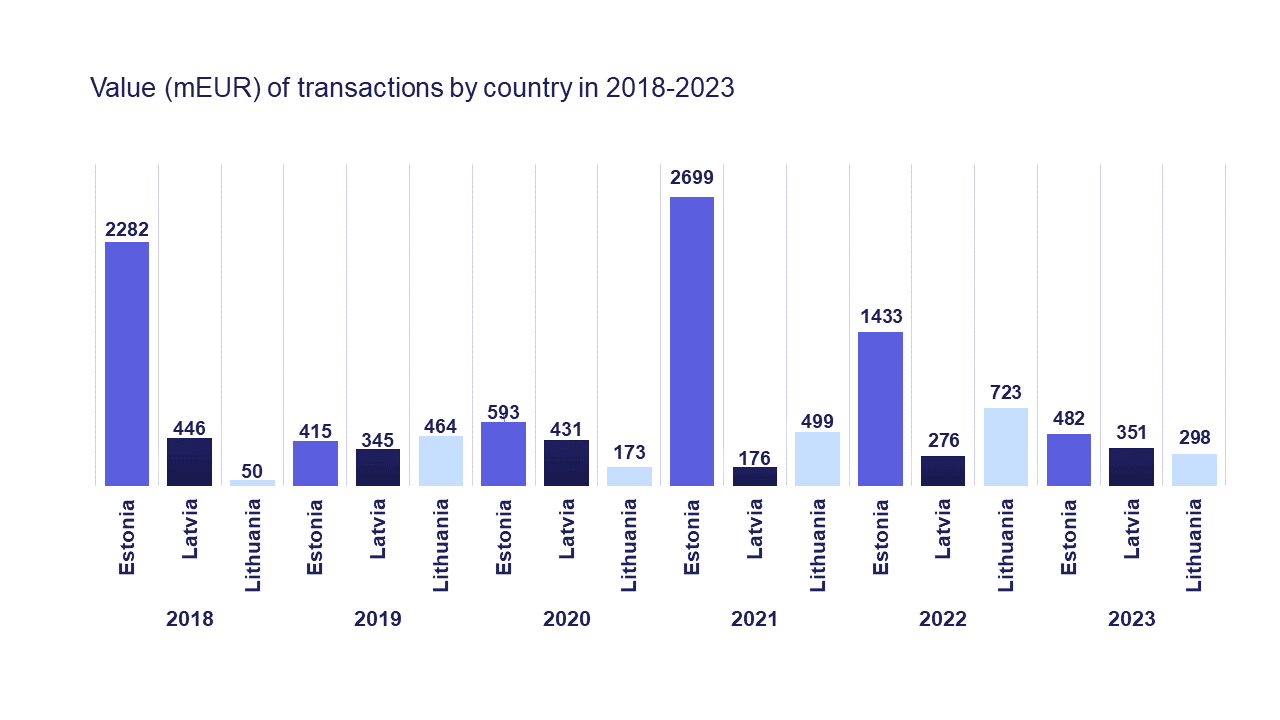

The tremendous drop in the disclosed deal values is the first thing that immediately becomes obvious when looking at Estonia’s statistics for 2023. The total value of EUR 482 million is barely a third of last year’s total disclosed transaction value, and not even a fifth of the 2021 amount.

The main reason for the drop in numbers is the record-breaking fundraising craze Estonian companies experienced two years ago. “Several unicorns and other large Estonian startups managed to raise significant funds in 2021 and the first quarter of 2022. This means they didn’t have to go through external financing rounds in 2023 after valuations plummeted,” Prangli comments.

The other factor somewhat eschewing the picture is the fact that Mergermarket data only includes disclosed transaction values. Contrary to what Mergermarket data suggests, the largest deal in the Baltics may have easily come from Estonia: namely, the deal that gave birth to a joint venture between the City of Tallinn and the private utility and energy company Utilitas. However, as the value of this deal remains undisclosed, it did not factor into the statistics.

Prangli notes that the number to watch more closely than the total deal value is the total number of transactions. No such bleak drops occurred in this category. Despite a decrease for two consecutive years, Mergermarket statistics still reveal a healthy deal activity that surpassed the years 2018-2020.

Foreign direct investment (FDI) controls, finally implemented in Estonia last year, had a very limited effect on the transaction market due to the limited scope of the control, according to Prangli. The regulations imposed the obligation to obtain an authorisation for investment by non-EU investors in strategically important areas falling under the scope of the regime. This includes providers of vital services (e.g. energy, transport and communications); as well as state-owned enterprises, manufacturers or suppliers of military goods and/or dual-use items.

Looking ahead we expect the Estonian deal market to at least maintain current levels, with a recovery in sight. There are many reasons to be hopeful:

- Some megadeals currently in the pipeline will be closed

- Cash-loaded venture capital is seeking targets

- Energy and technology sectors continue to enjoy high activity

- Founder and investor expectations for valuations are coming closer

- Recent unannounced insider rounds are bound to be followed by external rounds

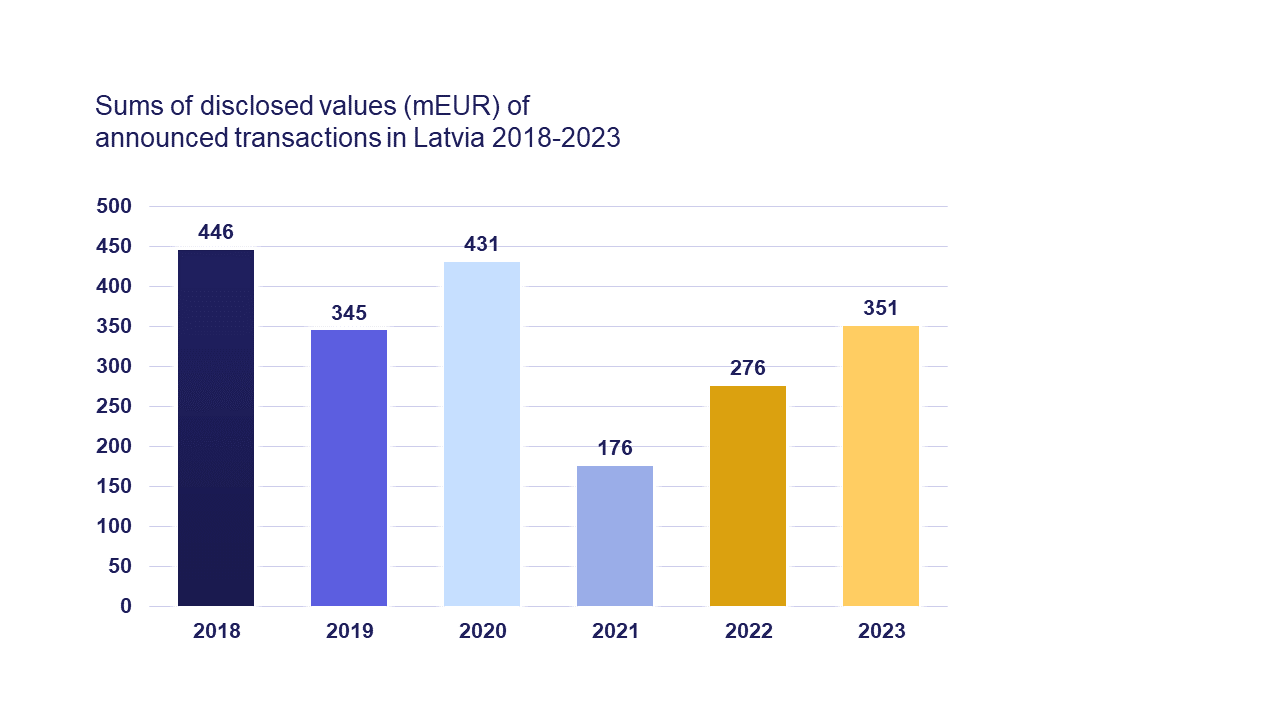

Latvia: massive gas deals set Latvia on positive trend

In Latvia the number of larger M&A deals with disclosed values has remained relatively stable, at just below 30, over the past three years. These numbers are significantly higher compared to pandemic-era levels.

The total value of larger announced deals continues to increase and is already approaching the earlier levels. After a significant drop in 2021, this seemed to be a faraway goal. The total deal value comes mostly from two large deals in the energy (natural gas) sector announced in 2023. Notwithstanding these two larger deals, the average deal value tended to decrease. It must be noted that the sale of Latvia’s Gaso to Estonian company Eesti Gaas is listed in the statistics as a Latvian deal.

The first half of 2023 remained rather slow in the Latvian market. This was mainly due to the ongoing war in Ukraine and financial shocks carried over from 2022, such as high inflation and a steep increase in interest rates. As soon as inflation levels normalised and market players began to adapt to the new circumstances, the market activity picked up in the second half of 2023. “Traditional M&A and private equity deals continue to dominate the Latvian market. The energy sector, especially renewables, remain dominant in Latvia,” partner Nauris Grigals notes.

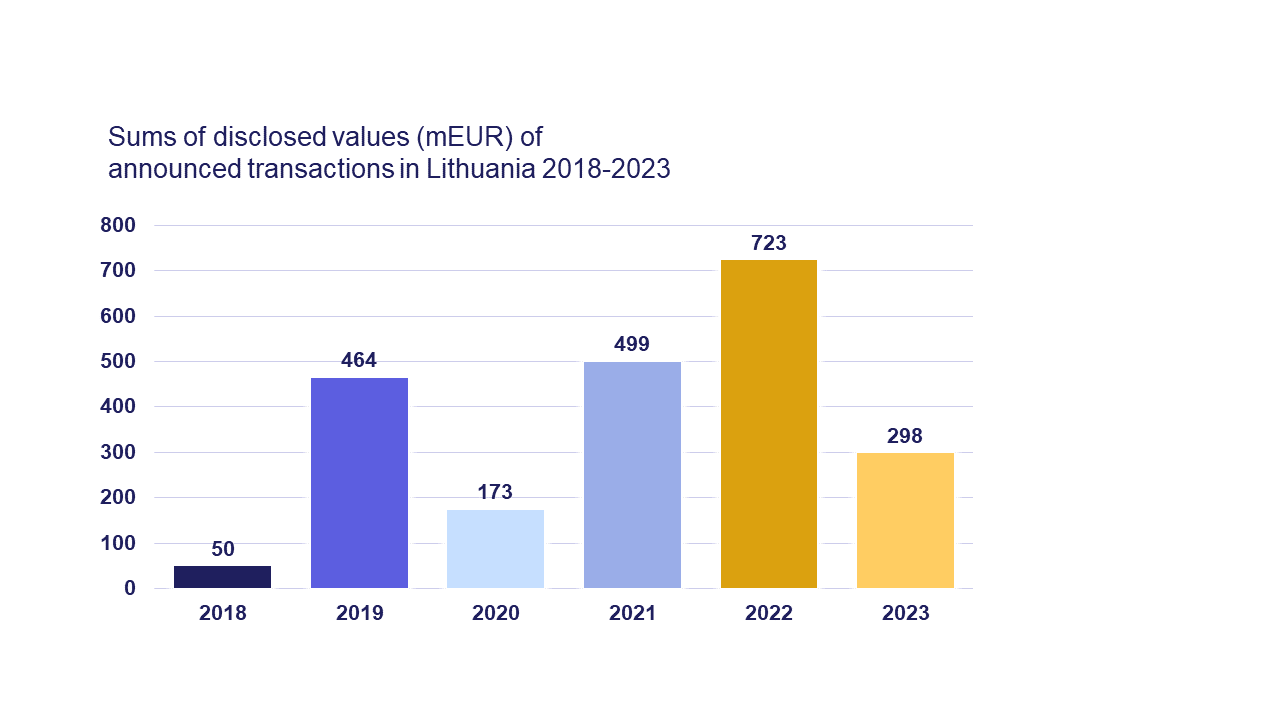

Lithuania: resilient economy emboldens local investors

Contrary to its Baltic neighbours, Lithuania avoided a recession in 2023. Supported by a resilient economy, Lithuanian buyers were actively investing in their own market with 43 deals of disclosed value to their name. Additionally, outbound investments made by Lithuanians included purchases made in Estonia (6 deals), Latvia and Poland (4 deals each), and the USA (2 deals). “We expect this trend to continue as the 2024-2025 economic outlook for Lithuania remains positive,” Laimonas Skibarka says.

The deal count remained stable, while transaction values – as far as the disclosed deals go – took a hit from EUR 723 million to EUR 298 million within a year. This also meant a smaller total than in the other Baltic markets.

As the deal count in Lithuania essentially did not drop in 2023, we can conclude that the impact of war has been minimal and we are past the initial shock. “The war in Ukraine may have postponed, or even caused the cancellation of some transactions, as it increased the country’s geographical risk profile,” Skibarka notes. “The period of fear, however, was rather short-lived.”

Register for Baltic M&A and Private Equity Forum!

The Baltic M&A and Private Equity Forum 2024 will be held in Vilnius at Saint Catherine’s Church on 16 April from 9:00 to 16:00, followed by an after-party. The special rate of EUR 308 + VAT will apply until 22 February with the promo code: SORAINEN_GNOZADsB

A well-established networking platform for Baltic transaction market players, the forum brings together 200+ participants each year. The event attracts private equity and VC funds, investment bankers, lawyers, advisers, company managers and shareholders.

Key topics this year:

- The European M&A market in the face of geopolitical turmoil

- Energy sector deals: what does the future hold?

- Private equity investments and exits today and tomorrow

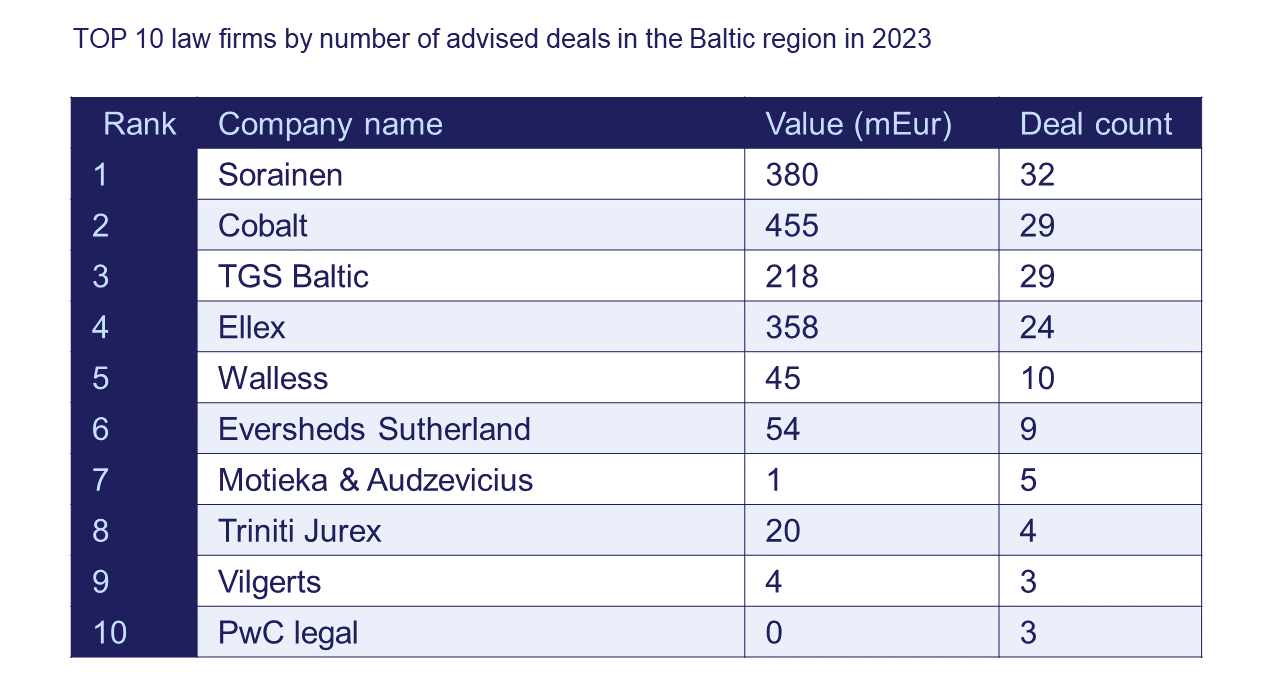

- The largest merger in the Baltics in 2023

- Impact of ESG on Baltic deals: exploring unused opportunities

- Merger filing: don’t make those costly mistakes!

- Deep look into notable recent Baltic transactions

Trusted M&A advisors at your service

For Sorainen, M&A and Private Equity is one of the key practices across the Baltics. Our firm has the experience, people, and skills necessary to handle the largest and most complex transactions in the region.

Contact our M&A and private equity experts for more info:

Toomas Prangli and Piret Jesse in Estonia

Eva Berlaus and Nauris Grigals in Latvia

Laimonas Skibarka and Mantas Petkevičius in Lithuania