Last year marked a revival for the Baltic M&A market, and we anticipate that 2025 will bring even stronger growth. The end of 2024 and the start of this year have been particularly intense for our M&A team, leaving us with an optimistic outlook!

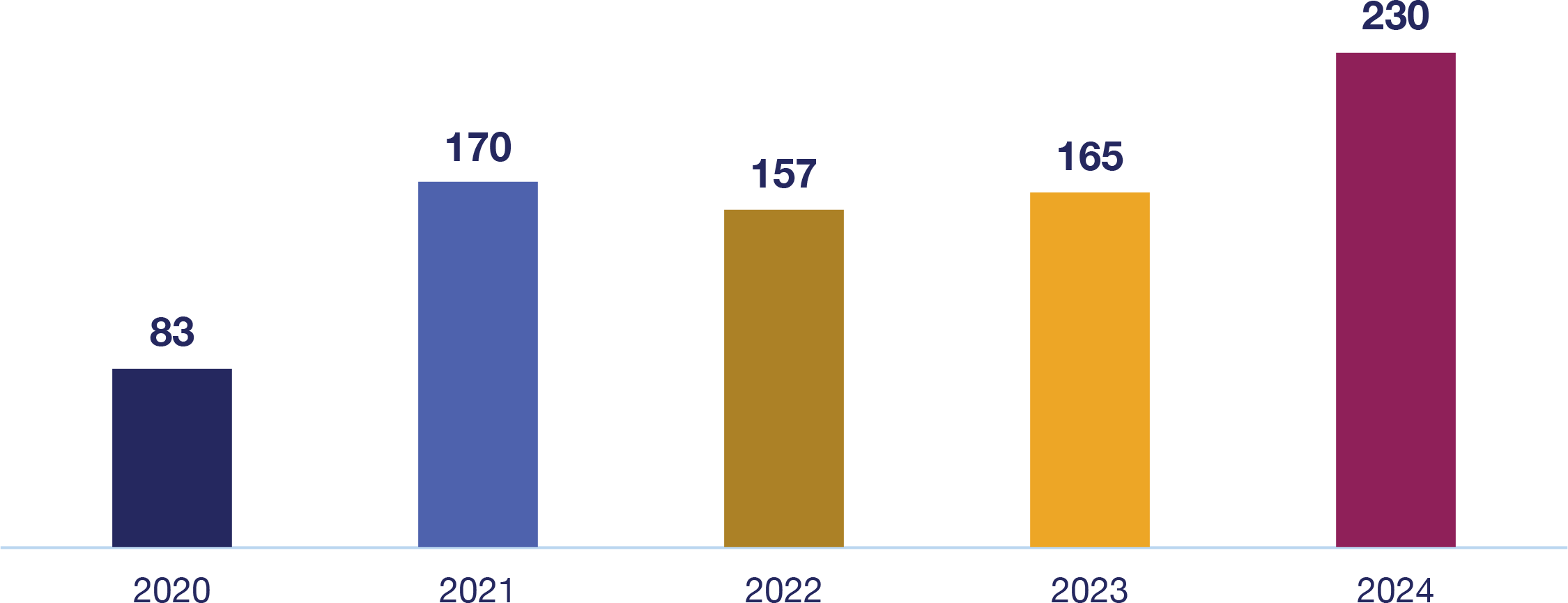

According to Mergermarket data, the total number of announced deals in 2024 grew by 39% compared to 2023, with disclosed deal values increasing even more, nearing the record levels of 2021–2022. Deal-making rose across all Baltic States, and the number of transactions with nine-digit values increased significantly: in 2023, there were only three deals at or above EUR 100 million, while last year, that number rose to seven.

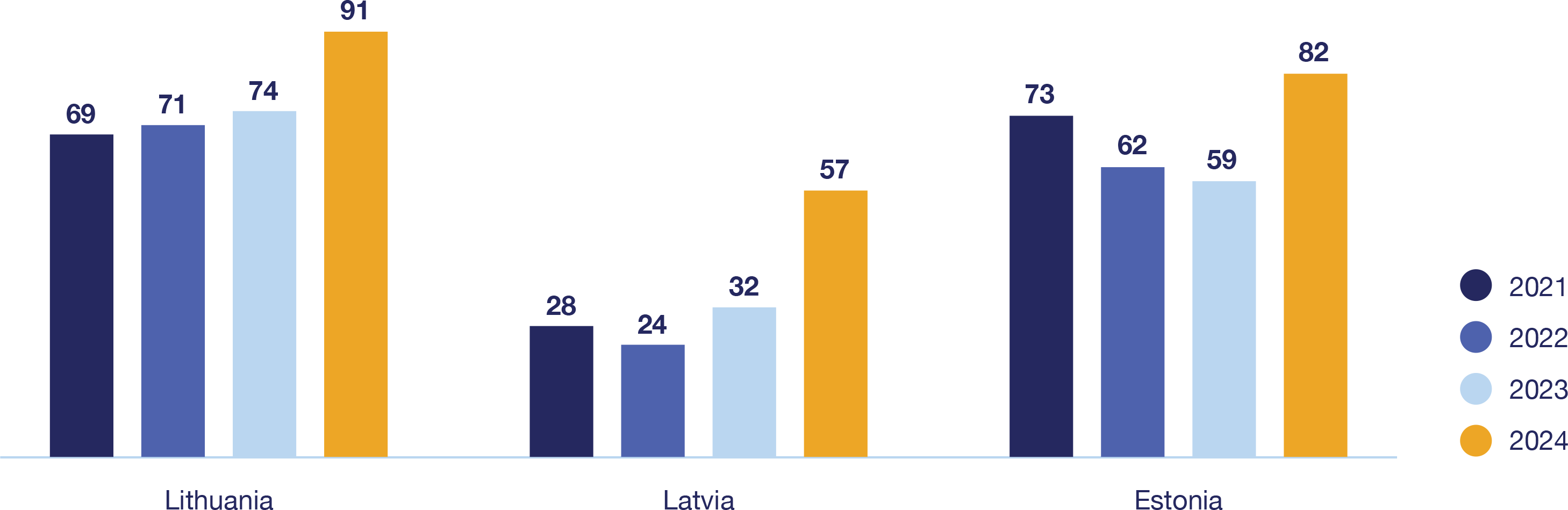

We expect the key drivers for Baltic M&A market growth this year to be the expanding Baltic economies, declining interest rates, and increased deal-making by private equity and venture capital players. In 2023–2024, several sale processes in the Baltics were postponed, or ongoing ones paused, due to geopolitical tensions, high interest rates, or the slowdown in the Baltic economies. That slowdown has now ended, and last year even Estonia’s M&A market (despite the country technically still being in recession in 2024) became more active – five of the Top 10 Baltic deals by disclosed value took place in Estonia, and Estonian investors participated in 45 Baltic deals, compared to 37 in 2023. Lithuania’s strong economic performance was also reflected in deal-making: another five of the Top 10 deals involved Lithuanian targets, and as many as 44% of deals with local (Baltic) investors were announced by Lithuanian buyers. As the Baltic economies return to growth, the financial results of Baltic companies will improve, making more businesses ready for sale.

Private equity remains among key drivers in the Baltics due to a pipeline of exits and acquisitions scouted by INVL Baltic Sea Growth Fund (which recently announced a successful exit from InMedica and is currently raising a new fund), Livonia, BaltCap and other PE players. We also observe a growing trend of Baltic businesses being passed on to the next generation (or sold) and this tendency is expected to increase in the coming years.

The share of deals by foreign (non-Baltic) investors increased from 40% in 2023 to 43% in 2024. We saw strong interest from Sweden (No. 1 with 15 deals), USA (14), Germany (12, which was No. 1 with 10 deals last year), UK (12), and Finland (9). We believe these trends will continue into 2025 as the Baltic economies return to a growth track and fears regarding geopolitical tensions recede.

Number of announced M&A transactions in the Baltics in 2020-2024

Source: Mergermarket

We note that until the end of 2022 Mergermarket statistics included only higher value transactions (normally exceeding USD 5 million), but the deal criteria were relaxed from January 2023 which resulted in a certain increase of reported transactions. Transactions have been allocated between countries based on “deal dominant geography” criteria in the Mergermarket database

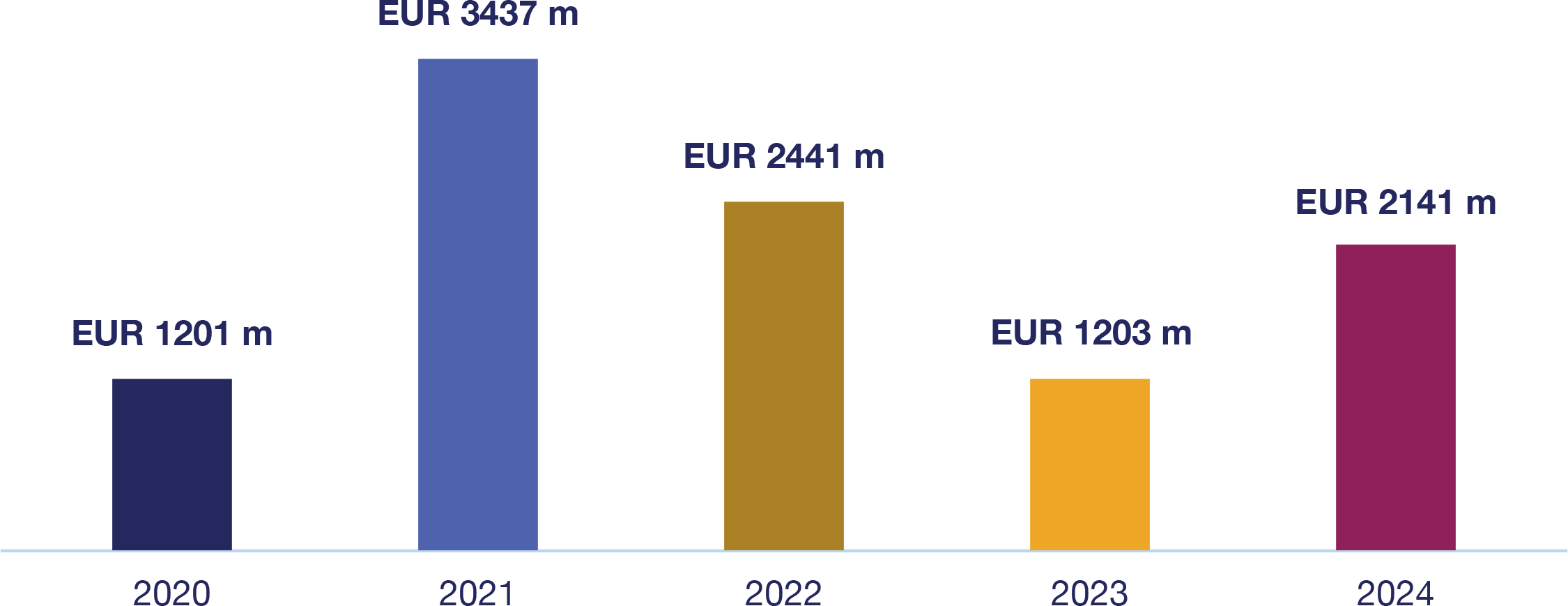

Sums of disclosed values of the announced M&A transactions in the Baltics in 2020-2024

Source: Mergermarket

We note that Mergermarket statistics include only values that were disclosed by deal parties to Mergermarket or publicly, thus the numbers in the table do not fully reflect the actual size of M&A market in the Baltics (and each respective country) and indicate only general tendencies

Number of transactions by country in 2020-2024

Source: Mergermarket

Number of transactions by country of investors in 2024

Source: Mergermarket

Lithuania leading the Baltic M&A landscape in 2024: record values, startup strength and a promising pipeline ahead

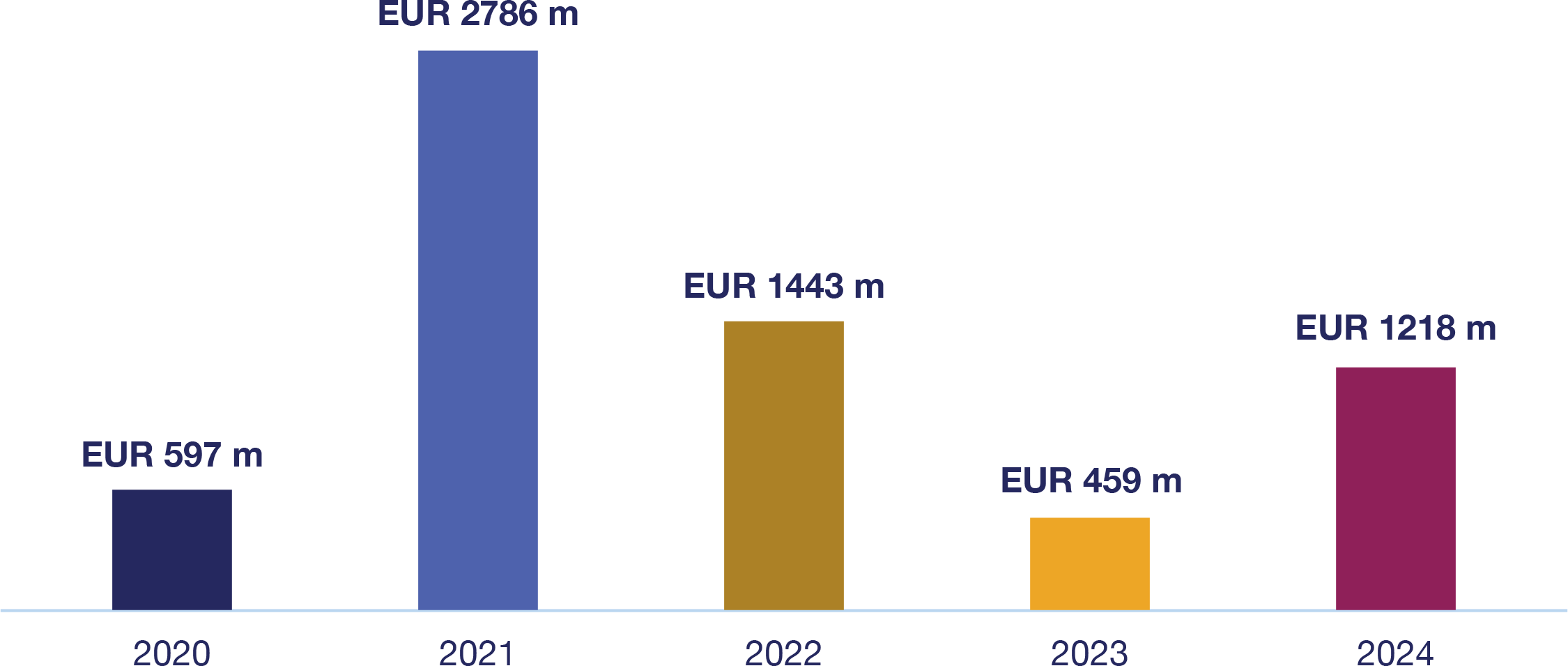

Being one of the fastest-growing economies in the EU last year, with GDP growth of ~2.5% in 2024 and ~3% forecasted for 2025, Lithuania stood out as the M&A powerhouse in the Baltics last year and looks promising for 2025 as well. Record total deal value, steadily growing deal count, five out of the Top 10 Baltic deals by disclosed value, plus the sizeable sale of Plasta and the recently announced InMedica, kept Lithuanian M&A advisers fairly busy. Sorainen Lithuania M&A team advised on signing six M&A deals during the pre-Christmas week alone, and the busy workload continued into January.

The most active sectors in Lithuania in 2024 were TMT, medical, financial services, and energy. In addition to these sectors, larger deals are expected this year in industrial/manufacturing and trade sectors. A few larger deals have been pending since last year (e.g. Luminor, Achemos Grupė, Cgates) and a number of new deals are in process or being prepared currently, and the general pipeline looks promising.

Private equity funds are fuelling the Lithuanian and Baltic M&A market well. For example, the core deal team of INVL Baltic Sea Growth Fund (which is now also raising a second fund with a EUR 250 million target size) is based in Vilnius and is thus fairly active in the Lithuanian market, but also looking across the Baltics and beyond (e.g. recently signed an acquisition of Pehart in Romania). Livonia completed its exit from Freor last year.

The Lithuanian startup ecosystem again showed its strength last year, fuelled by the record EUR 340 million secondary round in Vinted, EUR 20 million investment into Ovoko, the sale of Pixelmator Team to Apple, and others. The largest venture capital fund in the Baltics, Practica Capital, is also led from Vilnius and has been implementing exits in 2024 and will continue this year.

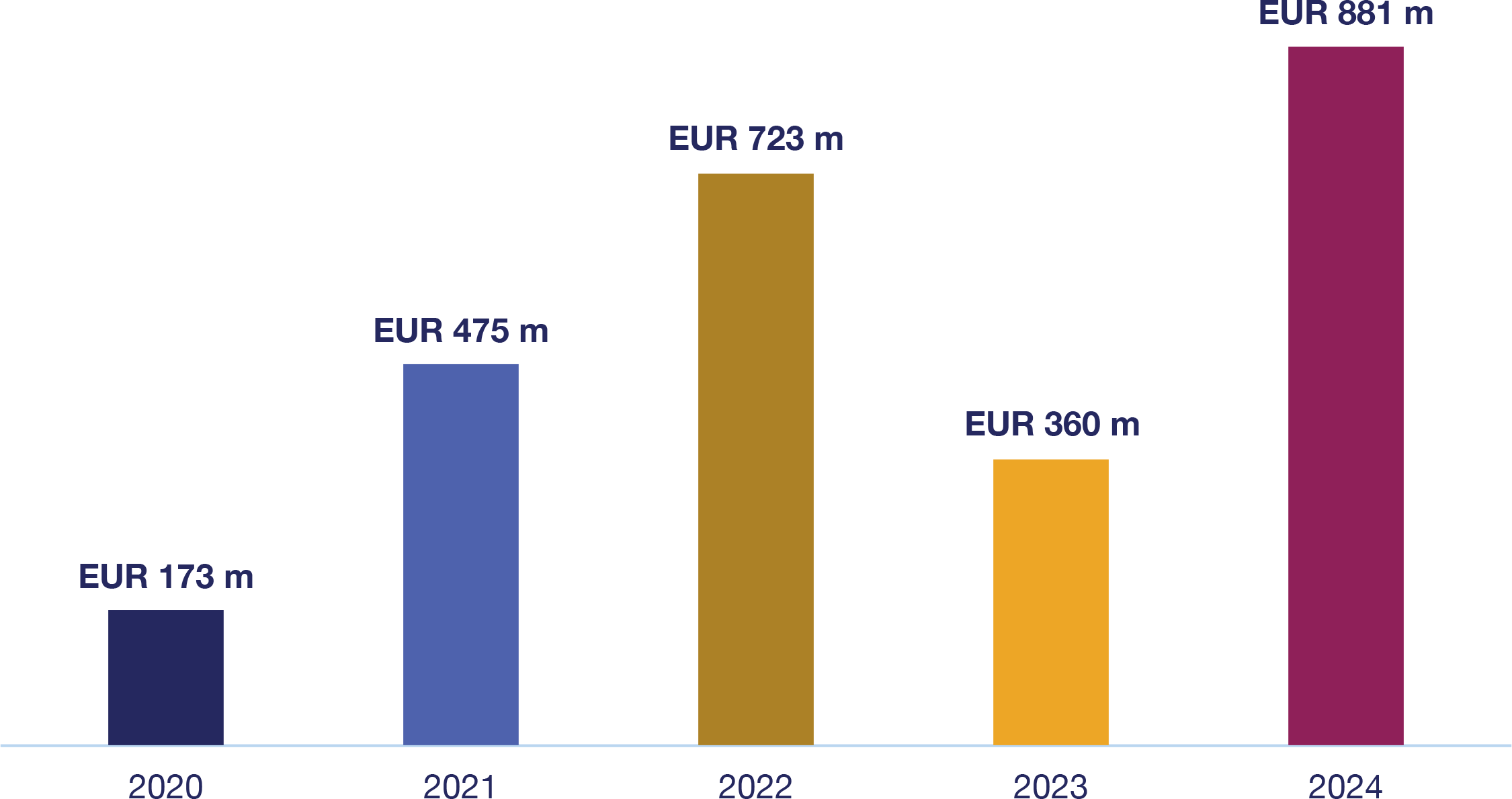

Sums of disclosed values of announced transactions in Lithuania 2020-2024

Source: Mergermarket

Estonia gradually emerging from recession: rising deal activity and local capital take centre stage in 2024

Despite the ongoing geopolitical tensions overshadowing foreign capital interest in the Baltics, the stabilisation of interest rates and availability of financing have positively impacted the market and enabled local capital to shine.

In 2024, Estonia gradually emerged from recession, leading to a significant increase in deal activity. The number of reported deals rose from 59 in 2023 to 82 in 2024, bringing it quite close to Lithuanian figures. Furthermore, reported deal values more than tripled, with five of Top 10 Baltic deals occurring in Estonia.

While the representation of foreign capital remains strong, we observe growing investments of local capital across all sectors and transaction sizes. Notably, two of Top 10 Baltic deals last year were based on Estonian local capital.

Overall, there was solid activity across all sectors, with TMT being the most active, followed by industrials and healthcare. The real estate sector also regained activity, with notable role of local capital. The largest real estate deals, such as the acquisitions of Viru Centre (retail), Kristiine Centre (retail), Port Artur (retail) and Technopolis Ülemiste (business premises), were all made by local capital. Both the energy and defence sectors, being among the fastest-developing industries, continue to attract investors and increasing deal activity.

Local private equity funds were waiting for a more favourable environment for exits, and their deal activity has been lower than expected, although some acquisitions can still be put on the account for 2024.

In capital markets, equity capital market was practically very slow in the Baltics last year, there were no IPOs in Estonia, other Baltic countries saw no large international deals either. However, the debt capital markets were quite active with Tier 2 bank bond issues (including LHV, BigBank and Holm Bank making its debut on the public capital markets). The government of Estonia as well issued a locally listed bond for the first time, targeting Estonian retail investors. The largest state-owned energy company, Eesti Energia, issued a hybrid green bond, the first of its kind on the Baltic market. The 2025 outlook for bond markets is perhaps not as active as last year. However, several roll-overs are expected. The IPO markets in Europe are slowly picking up but we do not anticipate much activity on Baltic market until Q3 2025. AirBaltic IPO in Latvia has been long awaited and, should it happen, might bring some increased activity also on neighbouring markets.

While several transactions remained on hold or encountered delays, we anticipate some of these will progress during this year. Additionally, the expected economic growth, cash-reloaded venture capital looking for targets, PE funds looking for exits and new targets, and a number of significant transactions in the pipeline suggest that 2025 will be even more active and should also bring growth in deal values.

The regulatory environment has remained largely unchanged, except that new debt pushdown rules have led to increased scrutiny by the Estonian Tax Board. In transactions, sanctions and ESG compliance screening have become increasingly important, alongside traditional areas of focus.

Sums of disclosed values of announced transactions in Estonia 2020-2024

Source: Mergermarket

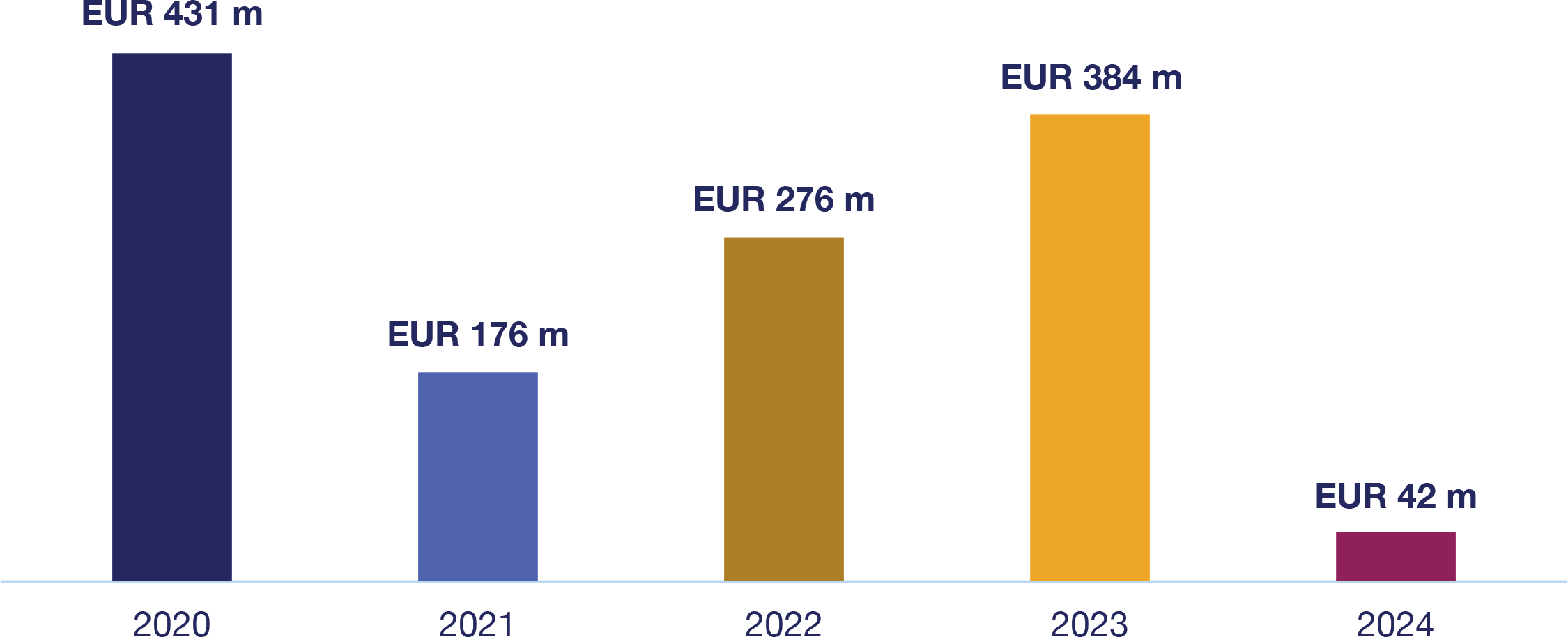

Record deal numbers in Latvia: smaller transactions pave the way for future growth

During the last couple of years, the number of reported M&A deals has grown steadily in Latvia, reaching a record number of 57 in 2024. This significantly decreases the gap between Latvia and its Baltic neighbours.

On the other hand, the positive trends and steady growth during 2021-2023 of the total disclosed value of deals has stopped and dropped abruptly to the lowest amount in years. Partially, this may be explained by the fact that for many deals the transaction value is not disclosed. For example, the mega-merger of Latvian unicorn Printful with its international competitor Printify didn’t credit anything to the Latvian deal value column. Nonetheless, the overall market also showed that the average value of M&A transactions in Latvia has decreased, especially in 2024. The Latvian market has been characterised by many smaller value deals rather than large deals with significant value.

Sector-wise deals in the energy/renewables sector continued to be one of the top sectors in the market. However, this market has significantly matured, and compared to the early boom years in 2021-2022, mature and developed projects dominate this market. The services and consumer sectors have been active in M&A in Latvia in 2024. We also see more succession/retirement-based transactions where entrepreneurs who established their businesses during the early independence years decide to exit.

The expected growth of the Latvian and, on a larger scale, the whole Baltic economies should feed an even more active M&A market in 2025. Current trends and the number and type of transactions in the pipeline give confidence to predict that 2025 will continue to be similarly active, with the addition of at least a couple of more significant deals topping the Baltic overall market, taking place in Latvia as well.

Sums of disclosed values of announced transactions in Latvia 2020-2024

Source: Mergermarket

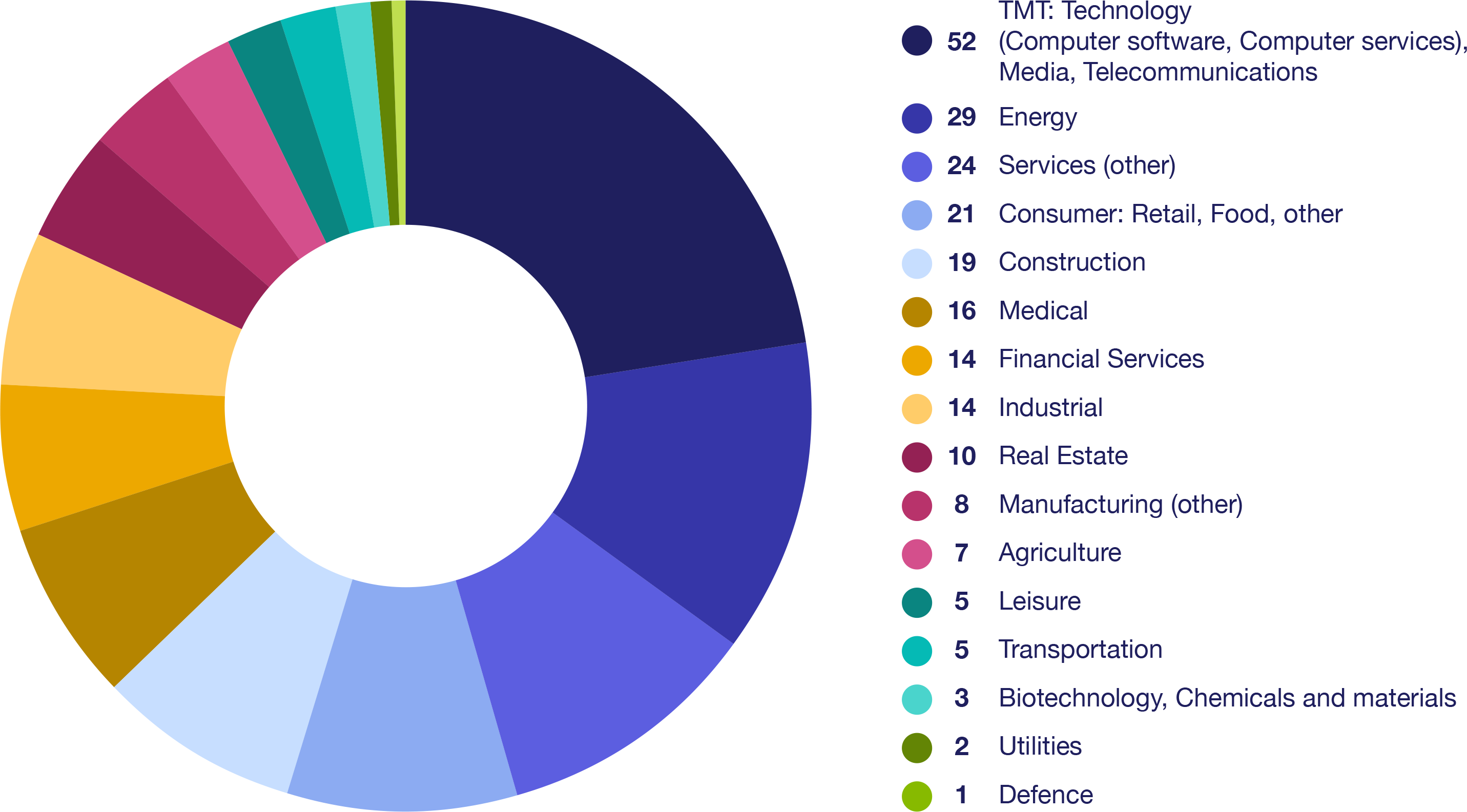

TMT sector continues leading the way

Pride of the Baltics – tech companies – remained the most attractive targets in 2024. The TMT sector has been the most active (No. 1 with 52 deals in 2024) for at least four years in a row, followed by energy (29 deals), services (24), and consumer (21). For 2025, we predict that the TMT, energy, and services sectors will continue to attract investors’ attention, and strong deal–making is expected in the industrial/manufacturing and trade-related sectors.

Source: Mergermarket

Thriving startup ecosystem in the Baltics: a year of milestones and exciting prospects

Among the Top 10 deals by value in 2023 there were as many as seven investments in startups and scale-up companies, while in 2024 there were four. But note that at least two significant startup deals did not make it to the Top 10 due to undisclosed values – the merger of Latvian unicorn Printful with its international competitor Printify and Apple’s announced acquisition of Pixelmator Team in Lithuania.

Notably, in 2024 Vinted closed a secondary share sale of EUR 340 million at a valuation of EUR 5 billion and is now the highest valued startup in Lithuania. From Estonian startups, Starship Technologies raised the largest round of EUR 90 million followed by Stargate Hydrogen with EUR 42 million.

Based on the announced deals, the Lithuanian ecosystem has made the most significant step forward by increasing the total amount raised in a year and attracting more investments than Estonian and Latvian startups. However, the number of startups that successfully raised funding in Estonia in 2024 surpassed those combined in Latvia and Lithuania.

We hope to see an upward trajectory in investment volumes in 2025, driven by the maturation of existing startups and the emergence of new ventures across various sectors (e.g. defence, AI, fintech, deep tech). Overall, the Baltics are proud of their thriving startup ecosystem and startup funding rounds and exits should continue.

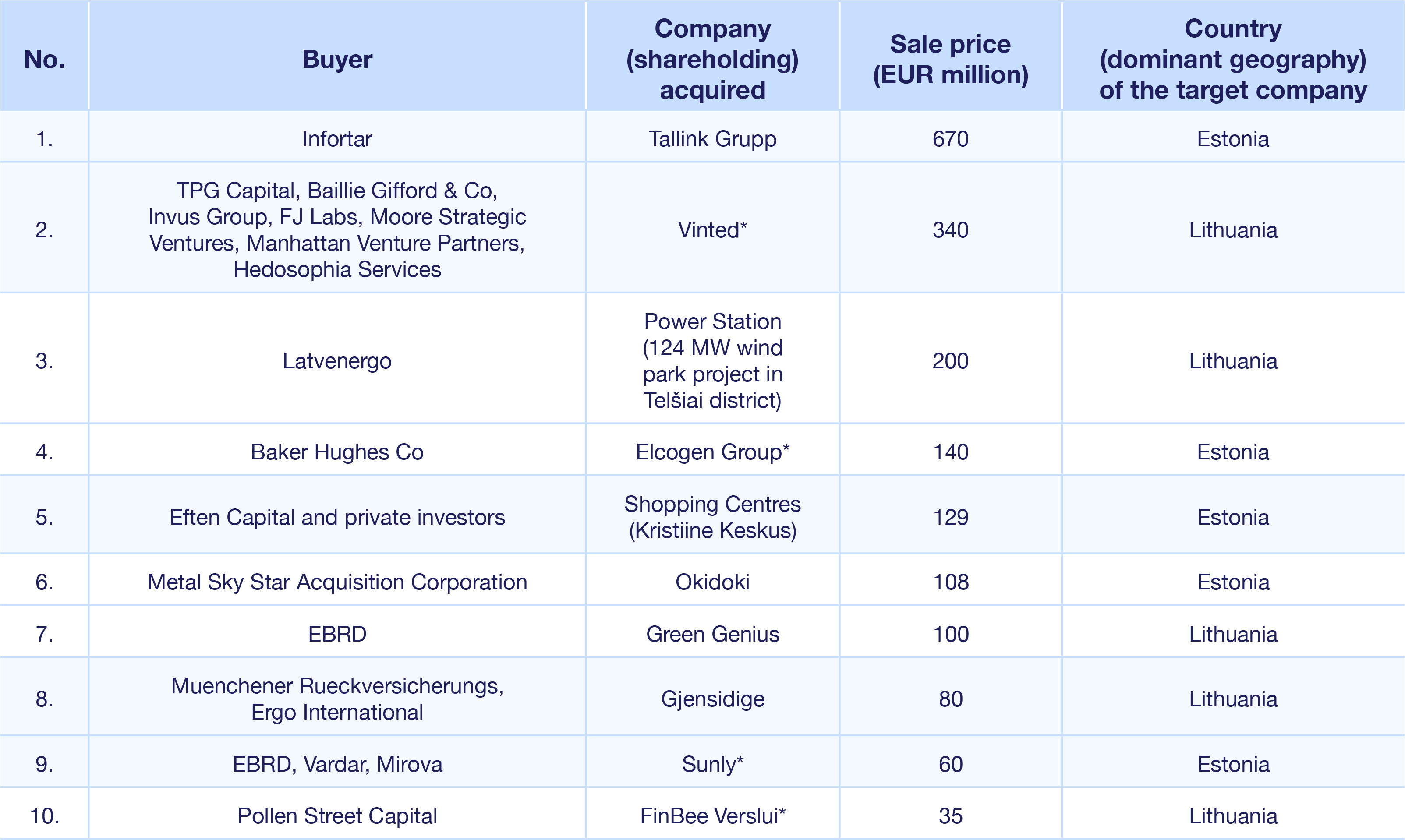

TOP 10 M&A transactions by disclosed sale price in the Baltics in 2024

* Start-up/scale-up companies

Deals advised by Sorainen highlighted with blue background

Source: Mergermarket and publicly available data

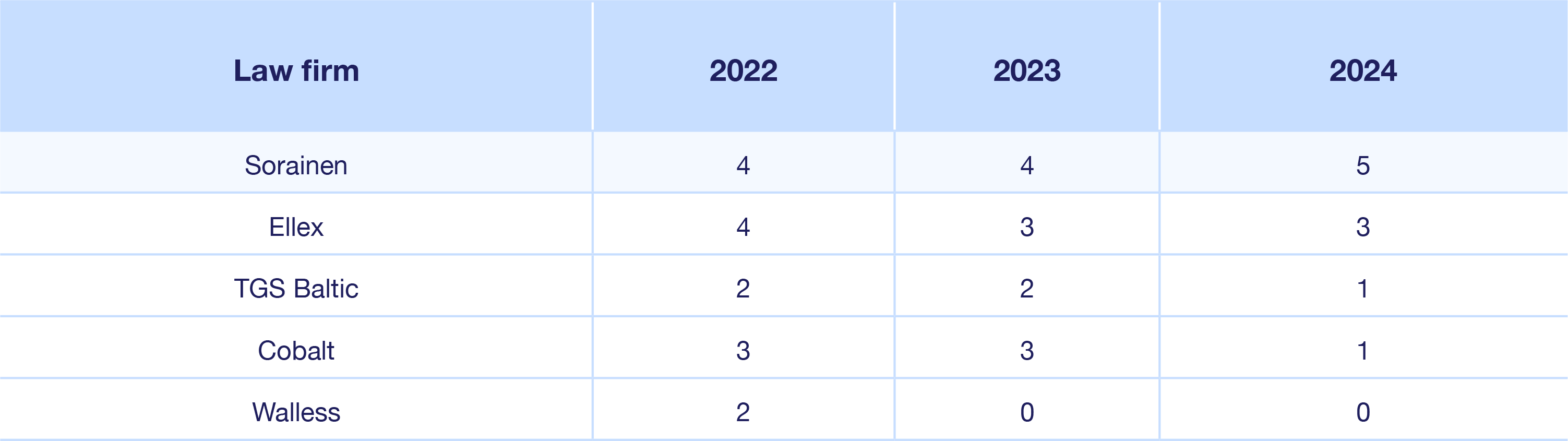

Baltic law firms/alliances by advised Top 10 deals in 2022-2024

Source: Mergermarket

Baltic Private M&A Deal Points Study 2024

The study analysed 179 private M&A transactions with a deal value of over EUR 1 million completed in the Baltics between April 2022 and March 2024 done in cooperation with other Baltic law firms under the auspices of the Estonian, Latvian, and Lithuanian Private Equity and Venture Capital Associations.

Let’s meet at the Baltic M&A and Private Equity Forum 2025!

The forum attracts 250+ participants from the Baltics and beyond and is a well-established annual industry event for the transaction market players: PE and VC funds, investment bankers, advisory industry, as well as company managers and shareholders.

View the programme HERE.

Register HERE.

Contact our trusted M&A and private equity experts for more info

- Laimonas Skibarka in Lithuania

- Piret Jesse and Mirell Prosa in Estonia

- Nauris Grigals in Latvia