Compared to the record level of dealmaking in the first half of 2024, the Baltic M&A market in H1 2025 slightly fell back in terms of transaction numbers, but total deal value surged, partly driven by increased startup activity. In the context of a steep decrease in the number of deals in EMEA (over -20% year-on-year according to Mergermarket data) due to tensions over international trade, the Baltic M&A market demonstrates resilience.

Market performance: momentum in Lithuania, stabilisation in Latvia and Estonia

Total deal count in the Baltics declined by 14% compared to the exceptionally active first half of 2024. However, deal activity was still 15% higher than in the same period in 2023, suggesting that the market is finding a new baseline. The total deal value jumped by as much as 67% due to one huge retail deal, as well as investments returning to the Baltics’ cherished startup sector.

Lithuania, demonstrating continuous strong economic development (GDP in Q1 up by +3.2% year-on-year, among the highest growth rates in EU), also recorded growth in M&A deal count (+17% compared to H1 2024). This was supported by steady investor interest, particularly in the software, energy and services sectors. Meanwhile, Latvia and Estonia experienced a slowdown in the number of deals following heightened activity in H1 2024. However, the two countries dominated the top 10 deals table, sharing all of the top six deals between themselves – in the retail, energy, technology and real estate sectors.

Number of M&A transactions in the Baltics in H1 2021 – H1 2025

![]()

Source: Mergermarket data as of 21 July 2025

Note that until the end of 2022 Mergermarket statistics included only higher-value transactions (normally exceeding USD 5 million), but the deal criteria were relaxed from January 2023, which resulted in a certain increase in reported transactions. Transactions are allocated between countries based on “deal dominant geography” criteria in the Mergermarket database.

Number of transactions by country in H1 2022 – H1 2025

![]()

Source: Mergermarket data as of 21 July 2025

Mega-deal drives surge in deal value

The total deal value for H1 2025 reached EUR 1.894 billion – a notably high figure driven primarily by Salling Group’s EUR 1.3 billion acquisition of Rimi Baltic. This single transaction accounted for nearly 70% of the total announced value for the period.

Sums of disclosed values of the M&A transactions in the Baltics in Q1 2021 – Q1 2025

![]()

Source: Mergermarket data as of 21 July 2025

Note that Mergermarket statistics include only values that were disclosed by deal parties publicly or to Mergermarket, and thus the numbers in the table may not fully reflect the actual size of the M&A market in the Baltics (or each individual country) and indicate only general tendencies.

Even excluding this outlier, deal values remained solid across several sectors, indicating that strategic transactions are still happening, albeit at a more measured pace. The presence of both local and international buyers suggests that the region continues to attract interest, though deal timelines have lengthened and execution has become more complex (similarly to other parts of the world).

Startup transactions return to centre stage

Between 2021 and 2023, startup and scale-up deals dominated the annual top 10 Baltic deal tables (making up five out of the top 10 in 2021, six in 2022 and seven in 2023), providing evidence of the thriving Baltic startup scene. But in 2024 this declined to four and remained lowish in Q1 2025, reflecting a tougher climate for startup funding worldwide. As a promising sign of recovering investor interest, all of the three deals appearing in the top 10 list for Q2 2025 are startup deals. As a result, we again see 50% of the 10 largest deals involving startup/scaleup companies.

In Latvia, Yeebet Gaming was acquired for EUR 106.59 million, while Aerones closed a financing round worth EUR 54.32 million. In Lithuania, Trafi (Intelligent Communications) was acquired for EUR 21.03 million, and Atrandi Biosciences attracted EUR 23.96 million in new capital. Estonia contributed with Blackwall’s EUR 45 million fund raising.

Top 10 M&A transactions in the Baltics by disclosed sale price in H1 2025

![]()

* Startup/scaleup companies

Transactions announced in Q2 2025 are highlighted in blue.

Source: Mergermarket and publicly available data. Transactions allocated between countries based on “deal dominant geography” criteria in the Mergermarket database.

These startup deals highlight recovering investor interest in deep tech, SaaS, advanced manufacturing and other startup segments in Baltics, though the broader startup ecosystem still remains sensitive to shifts in funding conditions.

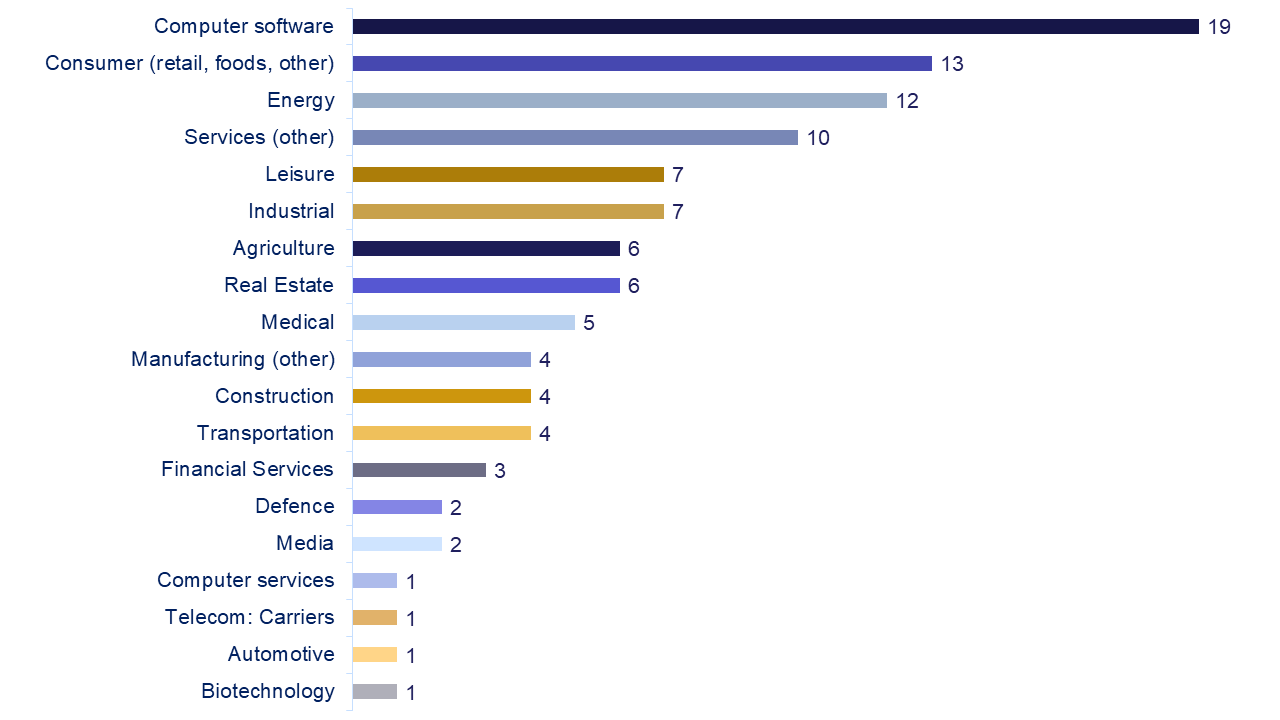

Sector overview: technology leads, consumer and energy follow

Technology remained the most active sector, with 19 software-related transactions plus one computer service deal. The consumer sector followed with 13 deals, including the abovementioned mega-deal. Energy (including renewables) and services remained robust, with 12 and 10 transactions respectively.

Other sectors, such as leisure, industrials and agriculture, were also reasonably active. Meanwhile, emerging areas like biotechnology and defence – though smaller in extent – suggest a gradual broadening of the regional M&A landscape.

Baltic M&A deals in H1 2025 by business sectors

Source: Mergermarket data as of 21 July 2025

We note that during the last two quarters a few larger infrastructure and energy deals were suspended or postponed due to geopolitical concerns (though these were cited usually in combination with case specific commercial issues). As a result, advisers and sponsors are increasingly interested in possibilities of softening these concerns with the help of political risk insurance solutions.

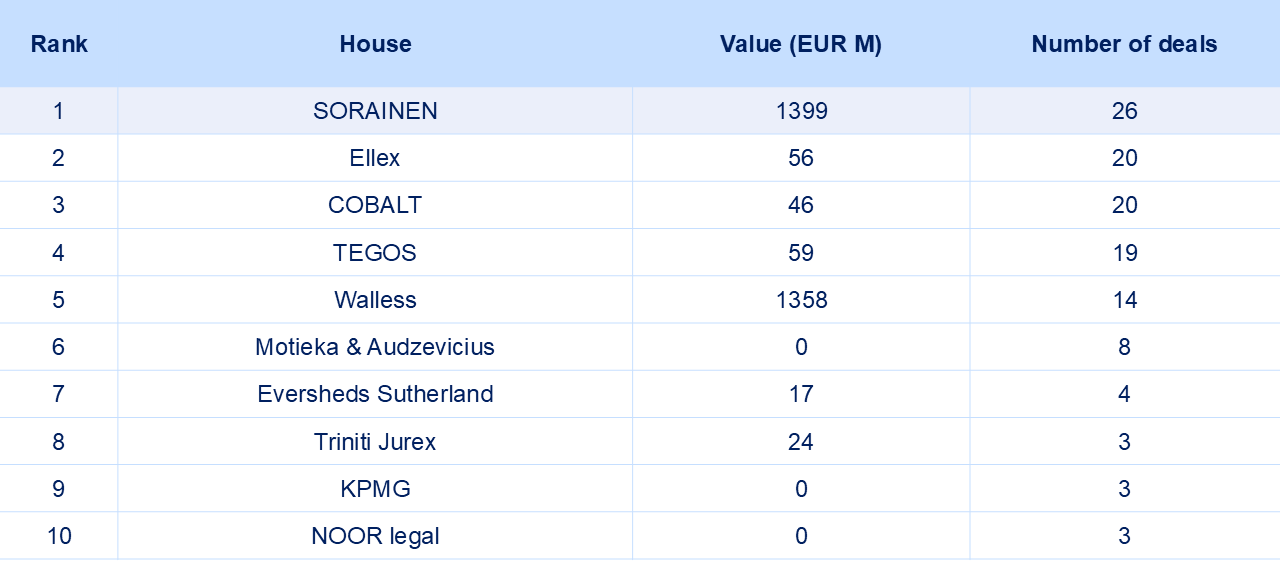

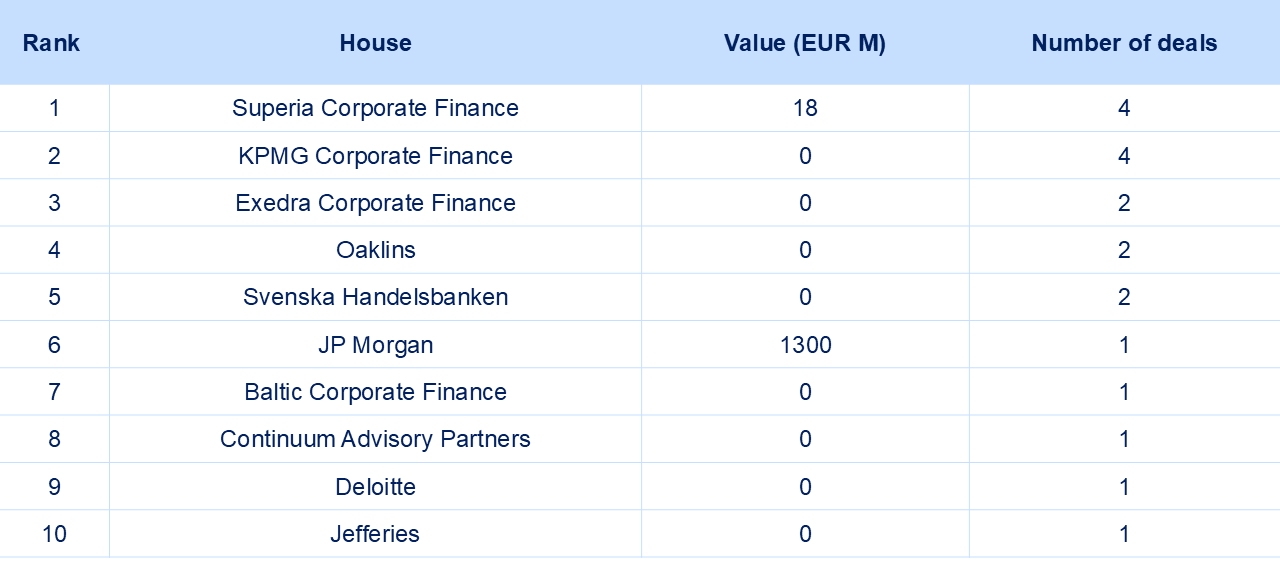

Key advisors: Sorainen maintains the top spot

Sorainen advised on 26 transactions with a combined disclosed value of EUR 1.399 billion, ranking first among M&A legal advisors in the Baltics both by deal count and value.

Explore the league tables of top legal and financial advisors in Baltic M&A deals below.

Top 10 law firms by advised deals in the Baltics in H1 2025

Top 10 financial advisors by advised deals in the Baltics in H1 2025

Source: Mergermarket data as of 21 July 2025

Conclusions and outlook

The first half of 2025 demonstrated the Baltic M&A market’s resilience and ability to adapt to changing conditions. While overall transaction volumes declined slightly (yet less than on the European market as a whole), the Baltic transaction market remained solid in key sectors and the total deal value grew as several high-profile deals were completed.

The re-emerging presence of startups among the top transactions suggests recovering investor interest in the Baltic tech innovators, though selective approaches are still more evident than in previous years.

Looking ahead to the second half of the year, the outlook remains moderate. While transactions are in progress and interest is strong in areas such as AI, cybersecurity, and defence, broader geopolitical and economic uncertainty continues to influence deal timelines and decision-making. If the UK and the EU complete their tariff deals with US reasonably soon, the European deal market should recover towards the end of the year which would also fuel the Baltic market.

As in other regions, investors and dealmakers in the Baltics are proceeding with greater scrutiny, and while opportunities remain, they are likely to be considered and pursued selectively. In this context, the Baltic M&A market appears to be entering a phase of greater deliberation, during which strategic alignment, sector resilience, and execution capability (including strong deal advisers) will play a greater role than earlier.

Contact our trusted M&A and private equity experts for more info

- Laimonas Skibarka, Mantas Petkevičius, Sergej Butov and Evaldas Dūdonis in Lithuania

- Nauris Grigals, Jānis Līkops and Eva Berlaus in Latvia

- Toomas Prangli, Piret Jesse and Mirell Prosa in Estonia